In the complex world of investing, it’s easy to get swept up in trends and rush to chase the latest stocks. But what if there’s a simpler, smarter approach for the long haul? I’m talking about buy-and-hold investing. This tried-and-tested strategy promotes patience and discipline, centered on acquiring high-quality stocks and holding onto them for the long term.

By resisting the urge to trade frequently or pursue short-term gains, buy-and-hold investors harness the power of compounding. This way they can also navigate market fluctuations with confidence.

In this guide, we’ll delve into the core principles of buy-and-hold investing. We’ll see how it can help us reach our financial objectives. Drawing wisdom from seasoned experts, we’ll emphasize the significance of identifying strong companies, diversifying portfolios, and maintaining steadfastness amid market swings.

Whether you’re a seasoned investor seeking to refine your strategy or a novice taking your first steps, this guide will help. It will equip you with the knowledge and tools needed to thrive with a long-term investing approach. Let’s delve into the world of buy-and-hold investing and unlock its potential.

Topics:

Point #1: Introduction

Investing is a powerful tool for reaching financial goals and growing wealth over time. However, the stock market’s complexity often leaves investors feeling lost. Many try timing the market or chasing hot stocks. But for novice investors, it will only add stress and uncertainty to the journey.

The buy-and-hold investing approach advocates patience and a long-term view. It’s about buying quality stocks and holding onto them for years, even decades, resisting the urge to trade frequently.

“Buy-and-hold investing is not a get-rich-quick scheme, but a get-rich-slow strategy that focuses on time in the market, not timing the market.”

Buy-and-hold investing involves acquiring high-quality stocks and holding them for years or decades. This way, the investor’s emphasis is on patience and fundamentals over short-term market trends. This strategy harnesses compounding, minimizing costs, and restricting emotional reactions to market fluctuations. This small-looking step ultimately leads to higher returns.

Pioneers like Benjamin Graham and Warren Buffett championed buy-and-hold investing. They preach long-term investing principles through the basic framework of value investing. Warren Buffett is often heard quoting, “Our favorite holding period is forever.”

John Bogle, founder of Vanguard Group, further popularized buy-and-hold investing with index investing. It further simplifies our long-term commitments to quality stocks.

How buy-and-hold investing could work for you? We’ll see how one can practice it. But before that, let’s brush up on a few basics first.

In the next part of this blog, we’ll delve deeper into the benefits of buy-and-hold investing and offer practical tips to implement this strategy effectively. Keep reading to elevate your investment journey.

Point #2: The Benefits of Buy-and-Hold Investing

Buy-and-hold investing involves buying stocks and holding onto them for many years. This strategy relies on the belief that, on a larger time frame, the market’s trajectory is generally upwards. Hence, short-term fluctuations in the market become less significant.

#2.1 Less Stress and Taxes

One of its key benefits is the long-term perspective it provides to its investors. It helps us to weather market ups and downs with less stress.

This approach also saves money as it involves fewer trades, reducing fees and taxes. Reduced transaction costs are a significant advantage of buy-and-hold investing. With fewer trades, investors save on brokerage fees, taxes, and other expenses that can eat into returns over time.

“Buy-and-hold investing is like planting a tree – it takes time, patience, and nurturing, but the rewards are long-lasting.”

By avoiding frequent trading, investors also sidestep emotional decisions that can lead to poor choices and costly mistakes. Patience and a measured approach help investors stay focused on long-term goals.

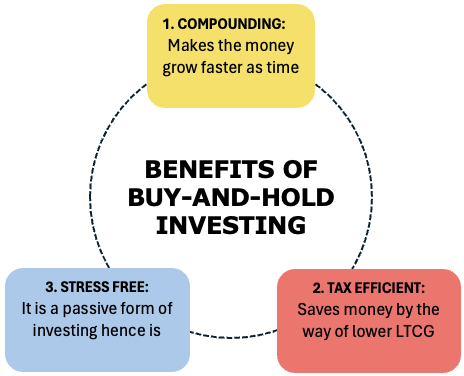

Buy-and-hold investing is simpler and less hands-on. This makes it attractive also for those who prefer a more passive approach to investing.

#2.2 Compounding

Compounding returns are another benefit. This means reinvesting earnings to generate more earnings over time, leading to exponential growth. By holding onto investments for longer periods, investors maximize compounding benefits.

For instance, if an investor puts Rs.5 Lakhs in a stock with an 18% p.a. annual return for 20 years. In this period, it could grow to around Rs.1.37 crore without any further trading.

| Data Input | |

|---|---|

| Initial Investment (Rs.) | |

| Expected Return p.a. (%) | |

| Time (in years) |

| Result | ||

|---|---|---|

|

Take another example of Ravi. He adopted buy-and-hold investing in 2004. He invested Rs.6,500 per month in an index fund. Despite market volatility, he continued his SIP for the next 20 years. During this period his portfolio grew to become Rs.85 Lakhs at 14% per annum. This type of hassle-free investing provides complete peace of mind.

Ravi’s story underscores the strength of buy-and-hold investing – a strategy not just for wealth creation but also for achieving emotional security and stability in investments.

Buy-and-hold investing helps avoid impulsive reactions to market swings, promoting disciplined and consistent returns over time.

#2.3 Tax Advantage

Tax efficiency is also notable. Holding investments for over a year qualifies for lower long-term capital gains tax rates, unlike short-term gains taxed at a higher rate.

When an investor holds an investment for more than one year, they become eligible for long-term capital gains tax (LTCG) treatment. This means that any gains realized after one year of holding an investment are taxed at a lower rate than short-term gains, which are taxed at a higher rate.

For example, in India, the LTCG tax on equity investments is 10% for gains over Rs. 1 lakh, whereas the short-term capital gains (STCG) tax is 15%. Read more about equity tax rules.

Point #3: Principles of Buy and Hold Investing

Experts stress the importance of having clear investing principles to guide decisions. These principles keep investors disciplined, focused, and less influenced by short-term market swings.

Following well-defined principles helps investors craft a long-term strategy aligned with their goals and risk tolerance. This fosters consistent, long-term returns while minimizing risks linked with speculative or short-term approaches.

Here are some essential principles for long-term investors:

- Invest in what you understand: It’s crucial to grasp the business or industry you’re investing in to make informed decisions and reduce risks.

- Diversify your portfolio: Spreading investments across various asset classes, sectors, and regions reduces risk by not relying too heavily on any single investment.

- Keep a long-term mindset: Short-term market movements can lead to emotional decisions. Focusing on long-term goals helps capture the benefits of compounding returns.

- Keep costs low: High fees and unnecessary trading can eat into returns. Minimize costs to maximize returns. Additionally, consider these principles for effective buy-and-hold investing:

- Invest in durable business models: Look for firms with strong, sustainable models that can weather market changes.

- Invest in companies with ethical and competent management: It refers to selecting stocks of firms led by trustworthy leaders with strong skills, integrity, and a commitment to long-term shareholder value. The business must be run with ethical business practices.

- Invest in companies with strong financials: Choose companies with healthy balance sheets, consistent earnings growth, and predictable future cash flows.

- Invest in companies with growth potential: It involves selecting stocks of firms expected to expand earnings and market share over time. If the aim is to earn higher returns, it will come from the future growth prospects of the company.

- Invest with a margin of safety: Buy undervalued stocks to minimize downside risk. The margin of safety refers to buying stocks at a price significantly below their intrinsic value. This reduces the downside risk. It acts like a cushion against potential losses.

- Invest with conviction: Hold onto high-quality stocks even during market downturns. Have an unwavering confidence in your chosen stock despite market fluctuations. Stay committed to them by believing in your thorough research.

These principles provide a solid foundation for successful investing. The emphasis on quality, patience, and discipline are the pre-requisite. Reflect on your strategy and consider incorporating these principles to achieve your financial goals. Remember, investing is a journey, and having a clear set of principles is the first step toward success.

Point #4: Identifying Quality Businesses for Long-Term Investing

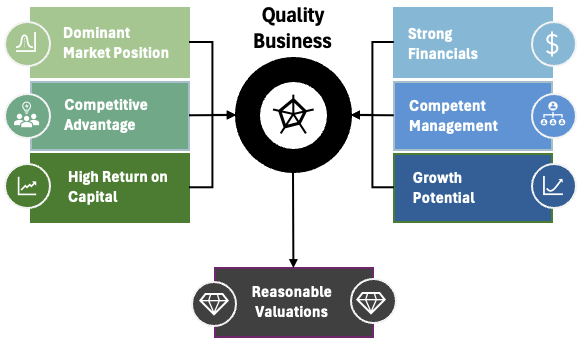

Recognizing quality businesses is vital for investment success as company performance drives long-term stock returns. Understanding what makes a business high-quality and selecting such companies is crucial for consistent returns amidst market volatility. This portion will explore the concept of quality businesses. Here, we’ll see the metrics and factors for identification.

A quality business exhibits traits like competitive advantage, financial strength, management quality, and growth potential. High-quality businesses maintain market position and profitability even during market fluctuations. Their dominance and sustainable competitive advantages ensure enduring success.

Identifying quality businesses is essential for successful long-term investing. Investors should seek companies with the following traits:

- Dominant market position,

- Sustainable competitive advantages,

- High return on capital,

- Strong financials,

- Competent management,

- Growth potential, and

- Reasonable valuations.

#4.1 Dominant Market Position

One way to identify a company with a dominant market position is to look at its market share. A company with a high market share in its industry is likely to have a dominant position.

For example, if a company has a 40% market share in a particular industry, it is likely a market leader. Additionally, investors can also analyze the industry structure to determine if the company has a sustainable competitive advantage over its competitors.

#4.2 Sustainable Competitive Advantage

Investors can analyze a company’s competitive advantage by looking at its moat. A moat is a sustainable competitive advantage that protects a company from competition. Economic moat: A company’s economic moat refers to its ability to maintain its competitive advantage over the long term. Some quantitative factors to consider include the company’s market share, brand strength, and pricing power.

- Industry-specific metrics: Different industries have different metrics that are relevant in assessing a company’s competitive advantage. For example, in the pharmaceutical industry, patents and regulatory approval can be important factors in determining a company’s competitive position.

- Customer loyalty: Companies with high customer retention rates and repeat business may have a competitive advantage over their peers. One way to measure customer loyalty is through customer satisfaction surveys.

- Cost advantages: Companies with lower costs of production may have a sustainable competitive advantage. Investors can compare a company’s cost structure to its peers to determine if it has a cost advantage.

- Intellectual property: Patents, trademarks, and copyrights can protect a company’s products and give it a competitive advantage. Investors can analyze a company’s intellectual property portfolio to determine its competitive position.

- The barrier to entry: Companies with high barriers to entry may have a sustainable competitive advantage. Investors can look at factors such as capital requirements, regulatory hurdles, and economies of scale to determine if a company has a strong barrier to entry.

#4.3 High Return on Invested Capital

One way to analyze a company’s returns on invested capital (ROIC) is to look at its financial statements. ROIC is calculated by dividing a company’s net income by its invested capital (total assets minus current liabilities). A high ROIC indicates that a company is generating significant returns on the capital it has invested. A company with a high ROIC may be a good investment opportunity. Read More about ROIC here

#4.4 Strong Financials

Investors can analyze a company’s financials to determine if it has a strong financial position. They can look at metrics such as revenue growth, profit margins, and debt-to-equity ratio to determine the financial strength of a company.

A company with a strong financial position is more likely to weather economic downturns and other challenges. Here are some metrics that investors can use to identify companies with strong financials:

- Return on Equity (ROE): ROE measures the company’s profitability relative to shareholder equity. A high ROE indicates that the company is using its shareholder funds efficiently.

- Debt-to-Equity (D/E) Ratio: This ratio compares a company’s debt to its equity. A lower D/E ratio indicates that a company has less debt relative to its equity, which suggests a stronger financial position.

- Current Ratio: This ratio measures a company’s ability to pay its short-term liabilities with its current assets. A high current ratio indicates that a company has enough current assets to cover its short-term obligations.

- Free Cash Flow (FCF): FCF represents the amount of cash a company generates from its operations after accounting for capital expenditures. A positive FCF indicates that a company has enough cash to invest in growth opportunities while still returning cash to shareholders.

- Gross Profit Margin: This margin measures the percentage of revenue that remains after deducting the cost of goods sold. A high gross profit margin indicates that a company is generating more revenue per rupee spent on its products.

It is important to note that no single metric can provide a complete picture of a company’s financial position, and investors should use a combination of metrics and qualitative analysis to make informed investment decisions.

#4.5 Quality Management

Investors can analyze a company’s management team to determine if it is of high quality. They can look at factors such as the track record of the CEO and the board of directors, as well as the company’s corporate governance policies. A company with high-quality management is more likely to make good decisions and create value for shareholders.

One can use the following metrics to assess the quality of management in listed companies:

- Promoter Holding: A high promoter holding indicates that the management has a significant stake in the company’s success, which aligns its interests with those of the shareholders.

- Track Record: Investors should look at the track record of the management team to assess their ability to create value for shareholders over the long term.

- Governance: The quality of corporate governance is also essential in assessing management quality. Investors should look at the company’s disclosure practices, board composition, and other governance-related factors.

- Capital Allocation: Companies that allocate capital efficiently and generate high returns on investments are likely to have quality management.

- Employee Engagement: The level of employee engagement and satisfaction can indicate the quality of management. High employee satisfaction suggests that the management team is focused on creating a positive work culture and promoting a long-term focus.

- Communication: Effective communication with shareholders is an important factor in assessing the quality of management. Companies that communicate clearly and transparently with their shareholders are likely to have better management quality.

#4.6 Growth Potential

Investors can analyze a company’s growth potential by looking at its industry and market trends. They can also analyze the company’s product pipeline and expansion plans. A company with strong growth potential may be a good investment opportunity.

Investors can judge the growth potential of a listed company by looking at various quantifiable metrics such as:

- Revenue growth: Examining the company’s revenue growth over the past few years can provide insights into its potential for future growth. A consistently growing revenue trend is generally a good sign.

- Earnings growth: Earnings growth is also a key metric to evaluate a company’s growth potential. Investors can look at a company’s earnings over the past few years to gauge its potential for future earnings growth.

- Market share: A company’s market share can indicate its growth potential. A company that is gaining market share in its industry may have a competitive edge over its peers.

- Total addressable market (TAM): Evaluating the size of a company’s total addressable market can provide insights into its potential for future growth. A company operating in a large and growing market has greater growth potential.

- Research and development (R&D) spending: A company that is investing heavily in research and development may have a higher potential for future growth. Increased R&D spending can lead to new products, services, or technologies that can drive growth.

- Capital expenditures (CapEx): A company’s capital expenditures can also provide insights into its potential for future growth. A company that is investing in new equipment, facilities, or technologies may have a higher potential for future growth.

#4.7 Reasonable Valuations

Investors can analyze a company’s valuation by looking at its price-to-earnings (P/E) ratio and other valuation metrics. A company with a low P/E ratio may be undervalued and represent a good investment opportunity. Investors can also compare a company’s valuation to that of its peers to determine if it is reasonably priced. Investors can use several quantitative metrics to judge the reasonable valuation of listed companies.

Here are a few metrics:

- Price-to-earnings (P/E) ratio: The P/E ratio is a popular valuation metric that compares a company’s stock price to its earnings per share (EPS). A lower P/E ratio indicates that the stock is relatively undervalued, while a higher P/E ratio indicates that the stock is relatively overvalued.

- Price-to-book (P/B) ratio: The P/B ratio compares a company’s stock price to its book value per share. Book value is the value of a company’s assets minus its liabilities. Like the P/E ratio, a lower P/B ratio suggests that the stock is undervalued, while a higher P/B ratio indicates that the stock is overvalued.

- Price-to-sales (P/S) ratio: The P/S ratio compares a company’s stock price to its revenue per share. A lower P/S ratio suggests that the stock is undervalued, while a higher P/S ratio indicates that the stock is overvalued.

- Dividend yield: The dividend yield is the annual dividend payment per share divided by the stock price. A higher dividend yield suggests that the stock is undervalued, while a lower dividend yield indicates that the stock is overvalued.

- Price-to-cash flow (P/CF) ratio: The P/CF ratio compares a company’s stock price to its cash flow per share. A lower P/ CF ratio suggests that the stock is undervalued, while a higher P/CF ratio indicates that the stock is overvalued.

Investors can use a combination of qualitative and quantitative analysis to identify quality businesses for investment.

Point #5. Valuing A Business: Principles & Techniques

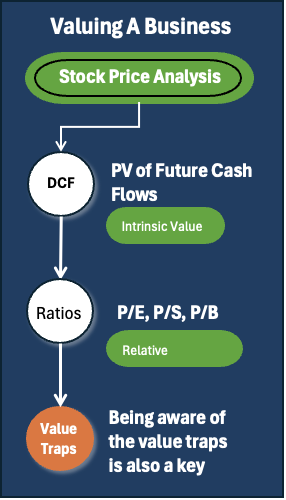

Valuing a business is crucial in investing. It’s about estimating the true worth of a company. The value is used to determine if a company is overvalued or undervalued. This one piece of information works as one of the biggest aids in smart investment decisions.

Understanding valuation is fundamental as it guides investors in identifying and avoiding good opportunities. Valuations help investors assess stock prices, determining if they’re justified, undervalued, or overvalued. This analysis is based on a company’s fundamentals and market position.

Discounted Cash Flow (DCF) analysis is a popular valuation method. It estimates the present value of a business’s future cash flows. To perform DCF analysis, investors forecast a business’s future cash flows. Then, these cash flows are discounted back to their present value using a suitable discount rate reflecting the investment’s risk.

DCF analysis requires assumptions about future growth rates and terminal values. It provides a systematic approach to valuing a business. As it is subject to uncertainties, it should be used alongside other valuation methods.

#5.1 Example

Let’s consider an example of a fictional company ABC Ltd. to demonstrate how to estimate its intrinsic value using the DCF method:

ASSUMPTIONS:

| SL | Description | Value |

| 1 | Current Year | 2024 |

| 2 | Free Cash Flow (FCF) | Rs. 10 Million |

| 3 | FCF Growth for the Next 10 Years | 5% p.a. |

| 4 | FCF Growth after the 10th Year | 3% p.a. |

| 5 | Discount Rate | 10% |

CALCULATION:

Let’s Calculate the present value (PV) of free cash flows for the next 10 years using the DCF formula.

PV of Future Cash Flows for the Next 10 Years

PV = CF1 / (1 + r) + CF2 / (1 + r)^2 + … + CF10 / (1 + r)^10

where, CF1 = Rs.10 million, r = 10% and CF2 to CF10 are calculated using the growth rate of 5%.

PV = 10 million / (1 + 10%) + 10.5 million / (1 + 10%)^2 + … + 16.7 million / (1 + 10%)^10 = 84.1 million

Terminal Value (TV) after the 10th Year

TV = FCFn x (1 + g) / (r – g)

where, FCFn = free cash flow in the 10th year, g = perpetual growth rate (3%) and r = discount rate (10%)

TV = 26.9 million x (1 + 3%) / (10% – 3%) = 372.7 million

Calculating the PV of TV

PV = Terminal Value / (1 + r)^10

= 372.7 million / (1 + 10%)^10 = 150 million

Add the present value of free cash flows and the present value of the terminal value:

Intrinsic Value = PV of Free Cash Flows + PV of Terminal Value

= 84.1 million + 150 million = Rs. 234.1 million

Therefore, based on these assumptions and calculations, the estimated intrinsic value of ABC Ltd. is Rs. 234.1 million. If the company’s current market capitalization is below the intrinsic value, it may be considered undervalued. However, if the current market capitalization is higher than the intrinsic value, it may be overvalued.

5.1 Relative Valuation

Relative valuation is another method of valuing a company by comparing its current valuation to that of other companies in the same industry or sector. This approach assumes that the market will value similar companies similarly. The differences in valuation can be attributed to differences in the company’s fundamentals.

One commonly used method of relative valuation is the Price-to-Earnings (P/E) ratio, which compares a company’s stock price to its earnings per share (EPS). A higher P/E ratio implies a higher valuation relative to earnings, indicating that investors are willing to pay more for each dollar of earnings generated by the company.

Another method of relative valuation is the Price-to-Sales (P/S) ratio, which compares a company’s stock price to its revenue per share. A higher P/S ratio implies a higher valuation relative to revenue, indicating that investors are willing to pay more for each dollar of sales generated by the company.

The Price-to-Book (P/B) ratio compares a company’s stock price to its book value per share. A higher P/B ratio implies a higher valuation relative to the company’s book value, indicating that investors are willing to pay more for each dollar of assets owned by the company.

Investors can use relative valuation methods to compare a company’s valuation to that of its peers or industry averages. For example, if a company’s P/E ratio is higher than its industry average, it may be considered overvalued relative to its peers. However, it’s important to note that relative valuation methods have their limitations and should not be used in isolation.

Other factors, such as the company’s growth potential, financial health, and competitive position, should also be taken into account when valuing a business.

5.2 Valuation Metrics For Difference Industries

Valuation metrics for different industries/sectors vary due to the unique characteristics of each industry. In the technology sector, for example, companies are often valued based on their revenue growth rates and price-to-sales ratios. In the consumer goods sector, companies may be valued based on their brand recognition and market share.

For financial services, valuations may be based on price-to-earnings ratios or price-to-book ratios, as the profitability of financial institutions is often linked to their ability to generate returns on invested capital. The Indian banking industry, for instance, is commonly valued using the price-to-book ratio, which compares the current market price of the stock to its book value per share.

Investors need to understand the unique valuation metrics of each sector and industry to make informed investment decisions. By analyzing sector-specific metrics, investors can identify undervalued companies with the potential for long-term growth.

Here’s a table summarising the valuation metrics for some of the top Indian industries:

| Industry | Valuation Metric |

| IT Services | P/E Ratio, EV/EBITDA, P/B Ratio |

| Pharmaceuticals | P/E Ratio, EV/EBITDA, P/B Ratio |

| Banking | P/E Ratio, Price/Book Ratio, Net Interest Margin (NIM) |

| Automobiles | P/E Ratio, EV/EBITDA, P/B Ratio |

| Oil & Gas | P/E Ratio, EV/EBITDA, P/B Ratio, Reserves Replacement Ratio |

| Consumer Goods | P/E Ratio, EV/EBITDA, P/B Ratio |

| Metals & Mining | P/E Ratio, EV/EBITDA, P/B Ratio |

| Telecom | P/E Ratio, EV/EBITDA, P/B Ratio, ARPU |

| Power | P/E Ratio, EV/EBITDA, P/B Ratio, Plant Load Factor |

| Real Estate | P/B Ratio, Net Asset Value |

It’s difficult to provide an acceptable range of valuation metrics for each industry as it can vary based on several factors such as market conditions, economic environment, company-specific factors, and so on.

However, as a general guideline, investors often use the following valuation metrics for different industries:

Acceptable Ratios:

| P/E ratio: | 10-25x |

| P/B ratio: | 1-4x |

| P/S ratio: | 0.5-3x |

| EV/EBITDA ratio: | 5-15x |

| NIM: | 3.30% |

| Reserve Replacement Ratio (RRR): | 1.2 to 1.7 |

| Average Revenue Per User (ARPU): | Rs.110 |

| Plant Load Factor: | 57% |

These ranges can serve as a starting point for investors to assess whether a particular company is overvalued or undervalued relative to its peers in the same industry. However, it’s important to note that each industry and company is unique, and investors should conduct a thorough analysis of the specific company and its industry before making any investment decisions.

5.3 Valuation Traps

Valuation traps refer to common mistakes investors make when valuing a company that can lead to poor investment decisions. Here are some common valuation traps to avoid:

Over-reliance on historical data: Using historical data to forecast a company’s future performance can be misleading.

A company’s past success does not guarantee future growth, and market conditions can change rapidly.

Ignoring industry trends: Ignoring industry trends can lead to inaccurate valuations. It is essential to understand the market dynamics, technological changes, and other industry factors that can impact the company’s growth prospects.

- Not factoring in the competitive landscape: Failing to consider the competitive landscape can lead to overvaluing a company. It is crucial to evaluate the company’s competitors, their strengths and weaknesses, and their market share.

- Blindly following analyst recommendations: Relying solely on analyst recommendations can be dangerous. Analysts can be biased, and their opinions can be influenced by factors other than the company’s fundamentals.

- Using inappropriate valuation metrics: Using inappropriate valuation metrics can lead to inaccurate valuations. For instance, using the P/E ratio to value a company in a capital-intensive industry may not be appropriate. It is essential to choose the right valuation metrics based on the company’s industry and characteristics.

By avoiding these valuation traps, investors can make more informed investment decisions and achieve better long-term returns.

Point #6. Building Gulak Portfolio

A Gullak Portfolio (Buy and Hold Portfolio) is a long-term investment strategy. Here, the investor selects a group of high-quality stocks and holds onto them for a minimum of 10 years. The term “Gullak” refers to the practice of physically storing stock certificates in a sealed container like a piggy bank. This process of physical handling of stock certificates reduces the temptation to trade frequently.

The benefits of Gullak Investing include reduced transaction costs, improved tax efficiency, and the potential for higher returns due to compounding over a long period. Additionally, the strategy allows investors to avoid the noise and short-term volatility of the stock market. Investors can focus on the long-term growth prospects of the selected companies.

The investment strategy involves selecting high-quality companies with a history of consistent earnings growth, strong competitive advantages, and a solid financial position. The portfolio should be well-diversified across sectors and industries to reduce risk.

Once the portfolio is constructed, the investor should hold onto the stocks for a minimum of 10 years without making any significant changes, thereby allowing the power of compounding to work in their favor.

“SMALL INVESTMENTS IN QUALITY COMPANIES, HELD FOR THE LONG TERM, CAN GROW INTO SIGNIFICANT WEALTH. GULLAK INVESTING TEACHES US THE POWER OF PATIENCE, CONSISTENCY, AND A SIMPLE APPROACH TO WEALTH CREATION.”

By treating our investments like a Gullak, we are taking a simple but effective approach to wealth creation. Just as you drop coins into a Gullak and forget about them, buy-and-hold investing requires the same mindset. Just buying high-quality stocks and holding onto them for years, even decades.

Mindset

Like a coin drop in a Gullak, imagine your stocks as your coins and investment portfolio (demat account) as your Gullak. These stocks of high-quality companies can grow into a fortune over time. What do you have to do? Just buy them and keep them shut, undisturbed for very long periods.

The key is to have patience, discipline, and a long-term perspective. Gullak investing teaches us that small steps taken consistently can lead to significant wealth creation in the future.

Building a Gullak Portfolio involves a systematic approach to investing. Identify a cost-intensive distant financial goal and then start accumulating stocks to support the goal.

Example

Say Rahul wants to build a Gullak Portfolio for his long-term investment. Before investing, Rahul needs to identify his investment goals and objectives. For instance, Rahul’s primary investment goal could be to save enough money for his child’s college education in the next 10 years. In this scenario, Rahul needs to consider the following factors:

- The current cost of a college education.

- Rate of inflation of college fees.

- The time horizon available for the goal.

After considering these factors, Rahul decides to invest in a diversified portfolio of blue-chip stocks with a focus on wealth accumulation. Rahul also decided to invest a fixed amount of money every month towards building his Gullak Portfolio.

Critical for Rahul here is to pick stocks with a bit of care. He must balance between growth and value stocks to build a well-rounded Gullak Portfolio. He should look for companies with sustainable competitive advantages, strong financials, and a history of steady growth. Factors such as industry trends, market share, and management quality must also be considered.

Read more about it in point #4 which deals in detail about “Identifying Quality Businesses for Long-Term Investing.”

Portfolio diversification is a critical aspect of building a Gullak Portfolio. Diversification helps to reduce risk and ensure that the portfolio is not overly exposed to any one particular sector or company. The portfolio should be diversified across various sectors and asset classes, including equities, bonds, and other investment vehicles.

Practicing Portfolio Diversification:

- Invest in companies from different sectors: Investing in a variety of sectors such as technology, healthcare, energy, financials, and consumer goods can help reduce the risk of concentration in a single industry. This ensures that if one sector underperforms, the impact on the overall portfolio is minimized.

- Invest in companies of different sizes: Companies of different sizes have different levels of risk and potential returns. Investing in a mix of large-cap, mid-cap, and small-cap companies can help balance the portfolio and mitigate risk.

- Invest in companies from different geographies: Investing in companies from different countries can provide exposure to different economies, currencies, and political environments. This can help reduce the risk of any one country’s economic or political turmoil affecting the entire portfolio.

- Invest in companies with different growth profiles: Investing in a mix of growth and value stocks can help balance the portfolio and provide exposure to different market cycles. Growth stocks tend to have a higher potential for capital appreciation but may be riskier, while value stocks tend to be more stable but with a lower potential for growth.

By diversifying the portfolio across different asset classes, sectors, and geographies, investors can reduce the risk of losses due to the underperformance of any one security or market segment. However, it is important to note that diversification does not guarantee profits or protect against all losses.

Balancing between growth and value stocks is an important consideration when building a Gullak Portfolio. Growth stocks tend to be higher risk and higher reward, while value stocks offer more stability and a higher dividend yield. The ideal portfolio should have a healthy mix of both growth and value stocks, depending on the investor’s risk tolerance and investment goals.

Balancing Between Growth and Value Stocks:

- Allocating a certain percentage of the portfolio to each category: One approach is to decide on a target percentage for each category and adjust the portfolio periodically to maintain that balance. For example, an investor might aim to have 60% of the portfolio in growth stocks and 40% in value stocks.

- Using a blended approach: Another approach is to invest in stocks that have both growth and value characteristics. These are often referred to as “Growth at a Reasonable Price (GARP)” stocks. This can provide exposure to both growth and value strategies in a single investment.

- Adjusting the balance based on market conditions: Market conditions can impact the relative performance of growth and value stocks. During periods of economic expansion, growth stocks may outperform, while during times of economic uncertainty, value stocks may perform better. An investor may choose to adjust the balance between the two categories based on their outlook for the market.

Ultimately, the key to balancing growth and value stocks is to remain disciplined and stick to the investment strategy, while periodically evaluating and adjusting the portfolio as needed to ensure that it continues to align with the investor’s goals and risk tolerance.

Building a Gullak Portfolio involves a disciplined approach to investing, with a focus on identifying high-quality companies with sustainable competitive advantages and a history of steady growth, while also maintaining a well-diversified portfolio and balancing between growth and value stocks.

Point #7. How To Monitor Gullak Portfolio

In the context of buy-and-hold investing, monitoring refers to the regular review and evaluation of the

performance of the stocks held in the portfolio. Monitoring is important for several reasons.

- Firstly, the stock market is dynamic and ever-changing. Companies that were once considered strong performers may face challenges and experience a decline in their financial performance. By monitoring the performance of the portfolio, investors can identify such trends early on and take appropriate action, such as selling underperforming stocks and reinvesting the proceeds in stronger performers.

- Secondly, monitoring allows investors to stay informed about industry trends and changes in the competitive landscape. By staying up-to-date with industry news and events, investors can make informed decisions about which stocks to hold in the portfolio and when to buy or sell them.

- Finally, monitoring is essential for assessing the overall performance of the Gullak Portfolio and whether it is meeting the investor’s goals and objectives. By regularly evaluating the portfolio’s performance, investors can identify areas for improvement and take corrective action if necessary. The risks of not monitoring the portfolio can be significant.

Without regular monitoring, investors may miss important changes in the fundamentals of individual stocks or the market as a whole. This can result in missed opportunities to sell underperforming stocks and buy more in stronger performers. Failure to monitor the portfolio can lead to poor investment performance and failure to achieve the investor’s goals and objectives.

“MONITORING PORTFOLIO REGULARLY IS LIKE TAKING THE CAR FOR A ROUTINE CHECKUP – IT ENSURES THAT EVERYTHING IS RUNNING SMOOTHLY AND ANY POTENTIAL ISSUES ARE ADDRESSED BEFORE THEY TURN INTO MAJOR PROBLEMS.”

The key performance indicators (KPIs)

The key performance indicators (KPIs) that investors can use to monitor the performance of their Gullak Portfolio include the following:

- Return on Investment (ROI): This measures the amount of return earned on the investment, typically expressed as a percentage of the original investment.

- Volatility: This measures the degree of fluctuation in the portfolio’s value. Higher volatility indicates greater risk.

- Sharpe Ratio: This measures the risk-adjusted return of the portfolio, by taking into account the amount of risk taken to achieve the return.

- Alpha: This measures the excess return of the portfolio compared to its benchmark.

- Beta: This measures the sensitivity of the portfolio to market movements. A beta of 1 indicates that the portfolio moves in line with the market, while a beta greater than 1 indicates that the portfolio is more volatile than the market.

- Maximum Drawdown: This measures the largest percentage decline in the portfolio’s value from its peak to its trough.

- Tracking Error: This measures the deviation of the portfolio’s returns from its benchmark (say Sensex). A higher tracking error indicates that the portfolio is less closely aligned with its benchmark.

Monitoring Schedule

It is recommended to monitor the Gullak Portfolio regularly, but not too frequently. The frequency of monitoring can depend on several factors, such as the investment horizon, the level of diversification, and the volatility of the portfolio.

For long-term investors, it may not be necessary to monitor the portfolio frequently. For such investors, the short-term market fluctuations are not too relevant. However, it is important to review the portfolio periodically to ensure that the original investment thesis is still intact.

On the other hand, investors with a shorter investment horizon or a higher level of portfolio concentration may need to monitor their portfolios more frequently. It must be done to manage risk and make timely adjustments as necessary.

Ultimately, the frequency of monitoring should strike a balance between staying informed about the performance of the portfolio and avoiding unnecessary trading activity.

Portfolio Rebalancing

Portfolio rebalancing is defined as the act of adjusting the portfolio’s asset allocation to bring it back to its original target allocation. The purpose of rebalancing is to maintain the desired risk and return characteristics of the portfolio over

time.

Portfolio rebalancing should be triggered by specific events, such as changes in market conditions, investment goals, or life events of the investor.

For instance, if a stock in the portfolio experiences a significant price increase, it may become overweight relative to the other holdings, and the portfolio may need to be rebalanced by selling some shares to maintain the desired allocation.

Rebalancing can be done regularly, such as annually or semi-annually, or on an as-needed basis. The frequency of rebalancing depends on the investor’s goals, investment horizon, and level of diversification.

A long-term investor with a well-diversified portfolio may only need to rebalance once a year, while a short-term investor with a concentrated portfolio may need to rebalance more frequently.

Here are some tools and techniques that can be used for monitoring the performance of an investment portfolio:

- Online Portfolio Trackers: There are several online portfolio trackers available such as Moneycontrol, and ET Money in India. These platforms allow investors to track their investments across different asset classes and provide real-time updates on their portfolio’s performance.

- The Stock Engine also allows users to add stocks to a portfolio or keep it on a watch list. Here, the user can view the key metrics of the stocks like their Overall Score and Intrinsic Value.

Point #8. Case Study

In 2011, Mr. Vijay Kedia invested in a little-known company called Cera Sanitaryware. The company manufactures bathroom fittings and fixtures. At the time, the company had a market capitalization of around Rs. 200 crore. Mr.Kedia had done his research and believed that Cera had a solid business model and a promising future in the growing Indian market.

Over the next few years, Mr. Kedia watched as Cera grew steadily. The company expanded its product line and distribution network. He held on to his shares, resisting the temptation to sell even as the stock price surged.

In March 2024, Cera had a market capitalization of around Rs.9,000 crore, a more than forty-fold increase from when Mr. Kedia first invested.

Mr. Kedia’s success with Cera is an example of the buy-and-hold approach to investing. He identified a high-quality company with a durable competitive advantage and a long runway for growth. He then held on to his investment for the long term. Mr. Kedia resisted the urge to trade in and out of the stock based on short-term stock movements.

“SUCCESSFUL GULLAK PORTFOLIOS ARE NOT BUILT OVERNIGHT; THEY ARE THE RESULT OF PATIENT AND DISCIPLINED INVESTING, STAYING COMMITTED TO LONG-TERM GOALS, AND ALLOWING TIME AND COMPOUNDING TO WORK THEIR MAGIC”

Case Study #2

HDFC Bank is one of the most successful banks in India. It has been a popular choice for long-term investment among Indian investors. The bank was founded in 1994 and has since then grown to become the largest private-sector bank in India in terms of market capitalization.

In 2005, a Gullak investor named Vivek Sharma invested in HDFC Bank with a long-term view. At the time of his investment, HDFC Bank was trading at a price-to-earnings (P/E) ratio of 25, which was considered high by many investors.

However, Vivek believed that the bank had a strong management team and a sound business model, which would allow it to grow consistently over the years.

Over the next 19 years, Vivek held on to his investment in HDFC Bank, despite market fluctuations and economic downturns. His patience and conviction paid off, as the stock price of HDFC Bank increased manifold, and the bank continued to report strong financials year after year.

As of March 2024, HDFC Bank’s P/E ratio stood at around 16. It delivered a compound annual growth rate (CAGR) of over 18.5% to its investors over the past two decades.

Vivek’s investment in HDFC Bank is a classic example of a Gullak portfolio. By investing in a high-quality company with a long-term view, he was able to reap the benefits of compounding over some time. His discipline and conviction helped him stay invested in the stock, despite short-term market fluctuations, and he was able to generate significant wealth for himself in the process.

Case Study #3

Another example of a successful Gullak portfolio is that of Eicher Motors, the parent company of Royal Enfield. In 2007, when Siddhartha Lal took over as CEO, Royal Enfield was a struggling motorcycle brand with limited appeal outside of India. However, Lal saw potential in the brand and decided to focus on quality and innovation, while maintaining the brand’s heritage and classic design.

Under his leadership, Royal Enfield launched new models, expanded its dealer network, and improved its production processes. These efforts paid off, as the brand’s sales and reputation grew both domestically and internationally.

In 2013, Eicher Motors decided to spin off Royal Enfield as a separate entity. Since then it has become a major player in the global motorcycle market. Investors who had included Eicher Motors in their Gullak portfolios in early 2013 would have seen substantial returns.

The stock has appreciated more than seven times since 2014. It has delivered an annual return of over 20% to its investors over the last 10+ years. The company’s success demonstrates the value of identifying quality companies early on and having the patience to hold on to them for the long term.

Case Study #4

Mr. Shukla, a software engineer from Bengaluru, started investing in the stock market in 2010 with an initial capital of Rs.5,00,000. He had heard about the concept of Gullak Investing and was intrigued by its potential. Mr. Shukla decided to start building a portfolio of stocks with a long-term perspective and minimal portfolio churn.

He started by identifying companies that had a consistent track record of revenue and earnings growth. He also looked for companies with a strong competitive moat and a high return on equity (ROE). After extensive research, he identified a few companies that met his criteria and started investing in them.

Over the years, he continued to hold on to these stocks and reinvested the dividends.

He also added more funds and bought new companies to his portfolio that met his investment criteria. Mr. Shukla made sure to diversify his portfolio across sectors. He made sure that will not put more than 5% of his capital in any single stock.

By 2024, in 14 years, his portfolio had grown to over Rs. 1 crore. A return of over 15 times on his initial investment. He had invested in companies such as TCS, HUL, and Bajaj Finance, among others. These companies had consistently delivered strong financial performance and had outperformed the market over the long term.

Mr. Shukla attributed his success to the principles of Gullak Investing, which had helped him stay disciplined and focused on the long term.

He believed that by investing in quality companies and holding on to them for the long term, he could build significant wealth and achieve his financial goals.

Case Study #5

This is about Gullak investing in volatile market times.

During the COVID-19 pandemic, the Indian stock market experienced high volatility, with sharp declines and recoveries in a short period. One investor, Mr. Kumar, had been practicing buy-and-hold investing for the past few years and decided to stick to his strategy despite the market conditions.

Mr. Kumar had invested in a basket of quality stocks with a long-term outlook. His picks were based on strong fundamentals, competitive advantage, and market leadership. He had diversified his portfolio across sectors and avoided the temptation to sell stocks based on short-term market movements.

When the pandemic hit, Mr. Kumar’s portfolio also experienced a significant decline, by more than 40%. However, he stayed disciplined and did not panic sell his holdings. Instead, he used the opportunity to add more shares of the companies that he had confidence in, as their prices had become more attractive.

As the market started to recover, Mr. Kumar’s portfolio also bounced back and delivered substantial gains. The stocks he held had strong fundamentals and had weathered the storm better than others. Moreover, he had added more shares at lower prices, which provided a boost to his returns.

Mr. Kumar’s Gullak Portfolio not only delivered excellent returns but also provided peace of mind during the volatile market conditions. By staying disciplined and focused on his long-term investment goals, he was able to navigate the market downturn and emerge stronger.

This case study shows that buy-and-hold investing can be an effective strategy even in a volatile market. By focusing on quality stocks and maintaining a long-term outlook, investors can weather short-term market movements and achieve their investment goals.

Key Takeaways

From these case studies of buy-and-hold investing discussed above, here are the key takeaways for prospective investors of the future:

- Long-term investment is crucial: The success of a Gullak Portfolio is largely based on long-term investments in high-quality companies with strong fundamentals.

- Patience is key: Investors must have the patience to hold onto their investments for long periods, even during times of market volatility or uncertainty. Diversification is important: Proper diversification of the portfolio can help mitigate risks and provide stable returns over the long term.

- Regular monitoring and rebalancing are necessary: Regularly monitoring the performance of the portfolio and rebalancing when necessary can help ensure that the portfolio remains aligned with the investment goals and objectives.

- Emphasis on fundamental analysis: Fundamental analysis of the company’s financial health, industry trends, and competitive landscape is necessary to identify high-quality companies with long-term growth potential.

The key takeaway from these case studies is that successful buy-and-hold investing requires a disciplined and patient approach, coupled with a focus on high-quality, fundamentally strong companies.

Point #9. Summing Up

Buy-and-hold investing stands as a steadfast strategy of the stock market. It has roots deeply planed in patience, discipline, and a focus on quality businesses. This approach emphasizes long-term growth over short-term gains.

The key for the investors is to identify high-quality companies. What are quality companies? One with sustainable competitive advantages, strong financials, and competent management. Such companies are more ready to weather market volatility and capitalize on compounding returns.

Valuation techniques such as Discounted Cash Flow (DCF) analysis provide a systematic approach to assessing the intrinsic value of businesses. It aids the investors in picking potential undervalued companies.

While uncertainties exist, buy-and-hold investing remains a cornerstone of wealth accumulation. It can offer stability, peace of mind, and the potential for significant long-term gains.

With a commitment to fundamental principles and a focus on the big picture, we ride the complex stock market with confidence.

Have a happy investing.

Suggested Reading: