Introduction

The United States has a fiscal deficit of around 6% of its GDP. It means that the US government is spending significantly more than it earns per year.

India, which is regularly criticised internationally for its fiscal management, keeps its deficit at around 4.4% of GDP.

Most developed economies aim for roughly 3%.

So the US is running a fiscal deficit of almost double the accepted benchmark. And yet, the US Dollar is the most powerful currency on the planet.

- Every central bank in the world holds dollars in its reserves.

- Every barrel of crude oil is bought and sold in dollars.

- Every major global transaction — trade, debt, investment — happens primarily in dollars.

The dollar has held this position for over 80 years without serious challenge.

This is the paradox.

A country that is technically spending far beyond its means is running the world’s most trusted currency. How? That is exactly what we’ll discuss in this post.

I’ll also explain how all of this connects directly to our stock portfolio here in India.

#1. It All Started With Gold

To understand why the dollar is king today, we have to go back in time.

For most of human history, paper currency had value because it was backed by gold.

If you held a currency note in your hand, it was essentially the government’s promise. It said, bring this note to any bank, and we will give you the equivalent amount of gold.

This system was called the Gold Standard.

It gave people genuine confidence. The paper in your wallet was not just paper. It represented actual gold sitting in a government vault somewhere.

That backing gave currencies their credibility.

But the Gold Standard had a limitation.

The economy could only grow as fast as your gold reserves grew. The government could not simply print more money to build roads, hospitals, or armies. No gold meant no money and no growth.

Then came the two World Wars. And they changed everything.

Countries needed to spend enormous amounts of money to fight those wars. Those expenditures were far more than their gold reserves could support. Hence, governments started printing money and borrowing heavily.

The Gold Standard began to crack under the pressure.

By the time World War Two was ending, most of Europe was in financial ruins. They had borrowed heavily and depleted their reserves.

The one country that came out of the Second World War in a position of real economic strength was the United States of America.

By 1944, the US held approximately two-thirds (67%) of the entire world’s gold reserves.

#2. The Bretton Woods Agreement

With Europe in ruins and the rest of the world needing to rebuild, there was an urgent need to design a new global financial system.

In 1944, representatives from 44 countries gathered in a small town in New Hampshire, USA, called Bretton Woods.

The agreement they reached was historic.

- Every country’s currency would be pegged to the US Dollar.

- And the US Dollar itself would be pegged to gold at a fixed rate of 35 US Dollars per ounce of gold.

- So in effect, all the world’s currencies became indirectly backed by gold, through the Dollar.

This made complete sense at the time, for three simple reasons.

- The US had most of the world’s gold.

- It had the largest economy.

- And it was the only country capable of providing that kind of financial stability to the rest of the world.

The world essentially said to the United States, “We trust you. We will link our currencies to yours.”

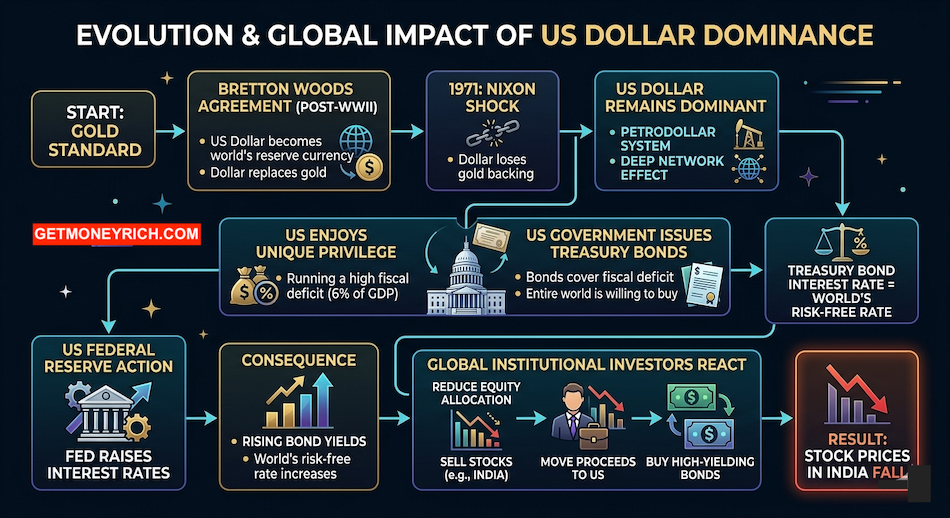

This was the moment (1944) when the US Dollar officially became the world’s reserve currency.

It was the formal beginning of Dollar dominance.

#3. The Day the Dollar Lost Its Gold Backing

The Bretton Woods system worked well through the late 1940s and 1950s. But cracks began to appear in the 1960s.

The US was spending heavily on the Vietnam War. It was also spending heavily on large domestic social programmes and on various other government expenditures.

To fund all of this, the US was printing dollars at a pace that made European countries uncomfortable.

France, in particular, became very suspicious. France had maintained large dollar reserves. And they wanted to test whether the US actually had the gold to back all those dollars they had been printing.

So France literally started sending ships to the United States, demanding gold in exchange for the dollars they held.

President Richard Nixon faced an uncomfortable reality.

The US did not have enough gold to honour all the dollar obligations it had made to the world.

So on the 15th of August, 1971, Nixon went on national television and made an announcement that shocked global financial markets. He suspended the convertibility of the US Dollar into gold.

Just like that, the link between the Dollar and gold was cut – that was the Nixon shock.

From that day onwards, the US Dollar became a fiat currency.

The Dollar now had value simply because the US government declared it had value. Not because of gold. Not because of any physical asset. Just a government declaration.

And since all other world currencies were pegged to the Dollar, they all became fiat currencies too.

At this point, the logical question is, if the Dollar is backed by nothing tangible, why did the entire world continue to trust it? Why did it not collapse?

The answer lies in what happened immediately after 1971 – a masterstroke of the US.

#4. The Petrodollar Effect

Post the Nixon Shock, the US handled the situation very cleverly.

In the early 1970s, US Secretary of State Henry Kissinger struck a landmark deal with Saudi Arabia. It was the most powerful member of OPEC at the time.

The arrangement was simple.

- Saudi Arabia and OPEC would price and sell all crude oil exclusively in US Dollars. Every barrel of oil sold anywhere in the world would be transacted in dollars only.

- In return, the US would provide military protection and weapons to Saudi Arabia. Those were the days when all Middle Eastern countries saw Israel as a security threat.

Think about what this meant for the Dollar.

Crude oil is one of the most critical commodities in the world. An industrialised economy cannot function without it. Every country needs it.

And if you want to buy oil, you first need US Dollars. So every single country on the planet now had a permanent, ongoing need to hold US Dollars.

The demand for Dollars became a necessity. This is what we call the Petrodollar System.

Earlier, countries held dollar reserves because the Dollar was pegged to gold. After 1971, they held dollar reserves because they needed dollars to buy oil. In a sense, gold was replaced — not by another metal, but by crude oil.

This is why, even today, when India buys crude oil from the Middle East, we pay in US Dollars. We are buying from an Arab country, with an Indian economy, but the transaction happens in dollars.

This is one big reason why the Indian Rupee is so sensitive to Dollar movements.

Hence, when the Dollar strengthens for any reason, it directly reflects as the Rupee weakening.

#5. The Network Effect

There is another force working in favour of the US Dollar that is even more powerful.

It is called the network effect.

Let me explain this with an example that every Indian will relate to immediately.

Why do most people in India use WhatsApp? Not because it is necessarily the best messaging app in the world. But because everyone else is on WhatsApp — your family, your colleagues, your clients, your vegetable vendor. If you want to communicate with anyone, they are already on WhatsApp. So you have no practical choice but to use it too.

And the more people use it, the more valuable it becomes. And the harder it gets to replace with something else.

The Dollar works in exactly the same way.

International contracts are written in Dollars.

- Oil is priced in Dollars.

- Gold is priced in Dollars.

- Central bank reserves are held in Dollars.

- When emerging market countries, including India, borrow money from international markets, that debt is mostly denominated in Dollars.

The entire financial infrastructure of the world has been built around the Dollar over the last 80+ years.

To shift away from the Dollar, you would need every country, every bank, every commodity market, and every financial contract in the world to agree to switch to something else simultaneously.

That is, for all practical purposes looks impossible right now.

So the Dollar remains dominant not only because of US economic strength, but because replacing it would require rebuilding the entire global financial system from scratch.

That is the depth of the network effect.

There is one more thing worth noting here.

- The US has the world’s most liquid financial markets US Treasury bond market and the US stock market).

- When there is fear or uncertainty anywhere in the world, global investors rush to safety. And in global finance, safety means U.S. dollars and US Treasury bonds.

- Even during crises created by the US itself (like the 2008 mortgage crisis, or the current US-Iran war), the Dollar actually strengthened.

- This happens because frightened investors worldwide bought more Dollars.

That tells you just how deeply rooted this dominance is.

If I had to estimate the weight of these two factors in keeping the Dollar strong:

- I would give the Petrodollar system about 35% and

- The Network Effect is about 65% in keeping the dollar strong all the time.

#6. The Fiscal Deficit

The US runs a fiscal deficit of about 6% of GDP; we know this, right?

Now, how does the US manage to keep its deficit so high without destroying its currency?

Before answering that, let’s know the basics:

- What does fiscal deficit mean?

- It simply means the government is spending more than it earns.

- The government earns money through taxes.

- If tax revenue is, say, 100 rupees but the government is spending 106 rupees, the shortfall of 6 rupees is the fiscal deficit.

For India, if we try to push our fiscal deficit significantly beyond 4.4%, the consequences will be like below:

- The credit rating agencies will downgrade us,

- Foreign investors will pull money out, and our currency will weaken.

Hence, we do not have the luxury of running a high deficit without facing market punishment.

The US runs a 6% deficit, and the world largely does not react. Why? There are three main reasons for this:

- First, the global demand for US debt. When the US government issues bonds to borrow money (to cover its deficit), there is always a queue of buyers. Japan, China, India, European central banks, etc., everyone holds US Treasury bonds as part of their foreign exchange reserves. Because of this guaranteed global demand, the US can borrow almost whenever it wants and at very low interest rates.

- Second, the US borrows in its own currency. Most countries that borrow internationally must borrow in Dollars. Only the US can control the Dollar, not the borrowers, right? If the Dollar strengthens, their debt burden automatically increases. But the US borrows in Dollars, which it can print. This is what economists call the “exorbitant privilege.”

- Third, institutional trust has been built over decades. The US has deep capital markets, strong institutions, a rule of law, and a long history of honouring its financial commitments. Trust accumulated over many decades does not disappear overnight, even if recent political developments are beginning to erode it.

#7. Government Bonds and the Risk-Free Rate

Now discuss how all of this directly connects to our investments. How, what happens in the US and to its Dollar affects us?

When a government needs to borrow money, it does not visit a bank the way you or I would. It issues bonds.

- In the US, these are called Treasury bonds.

- In India, they are called Government Securities, or G-Secs.

A government is considered the safest possible borrower. Why? Because it can, in theory, always print money to repay debt. Hence, the interest rate on government bonds is treated as the baseline safe return. In financial theory, this is called the risk-free rate.

The risk-free rate is the minimum return a rational investor will accept.

If I can earn 7% risk-free simply by buying a government bond, why would I put my money into stocks or mutual funds?

Yes, I can borrow elsewhere, but for that, I must get a return of more than 7%. Otherwise, it would not make sense to take extra risk for the same or lower return.

So the risk-free rate effectively sets the floor for all expected returns across the entire financial system.

Because US Treasury bonds are the gold standard of safe investments globally, the US 10-year Treasury yield is watched by every investor, every fund manager, and every central bank in the world.

- Before the pandemic, this yield was around 1.3%.

- Today it is around 4.3% — nearly a 3.5x jump.

That shift has had enormous consequences for every market in the world, including India.

This is one of the main reasons why, since the pandemic, US markets have performed so well, and other emerging markets like India and China have relatively struggled.

But we must also remember that high bond yield scenarios are non-sustainable.

#8. Equity Risk Premium

Here is the connection that I think every equity investor in India must understand.

It is called the Equity Risk Premium, and it explains exactly how bond yields affect your stock portfolio.

When you invest in equities (whether direct stocks or equity mutual funds), you are taking on genuine risk.

- The economy might slow down.

- The company might underperform.

- The stock price might fall.

- You are not guaranteed any return.

So a rational investor will only put money into stocks if they expect a return that is higher than the risk-free rate.

The extra return you demand from equities over and above the risk-free rate is the Equity Risk Premium.

The formula is simple:

Equity Risk Premium = Expected Return from Equities − Risk-Free Rate

Now think about what happens when the risk-free rate rises.

- Say earlier, the bond yield was 4% and equities were expected to return 10%.

- The equity risk premium was 6%.

- We can say that investors were getting 6% extra for the risk they were taking, and they seem to accept this 6% differential.

Now suppose bond yields rise to 7%. For equities to still offer the same 6% premium, they would need to return 13%.

But if the economy is slowing down because of high interest rates, companies are not going to suddenly start earning 13% more.

So one of two things must happen.

- Either investors accept a lower risk premium, or

- Stock prices fall to a level where the future return potential again becomes 13% or higher.

In most real-world situations, stock prices fall.

This is why, when the US Federal Reserve raises interest rates and bond yields rise, stock markets globally, including our Nifty and Sensex, declines.

Now you might think:

- I do not track US bond yields, so how does this affect me?

- The answer is that you, as a retail investor, are not the one moving the market.

- The market is moved by institutional investors:

- Mutual funds,

- Pension funds,

- Insurance companies,

- Sovereign wealth funds, and

- FIIs.

These institutions manage tens of thousands of crores of rupees. When we invest, we do so only in thousands or some lakhs.

Institutional investors have investment mandates that are benchmarked against the risk-free rate. When US bond yields rise by even 0.25%, these institutions recalculate their asset allocation models. So what do they do?

- They shift money out of equities and into bonds.

- And when large institutions move money, markets move.

- Even a 0.25% change in bond yields can trigger selling worth thousands of crores in equity markets.

This is why Indian markets fall every time the US Federal Reserve signals a rate hike. It is not panic. It is a systematic, financially logical chain reaction.

#9. The Full Cycle

- It starts with gold.

- After World War Two, the Dollar replaced gold as the world’s reserve currency through the Bretton Woods Agreement.

- In 1971, the Dollar itself lost its gold backing under Nixon.

- But the Dollar remained dominant because of the Petrodollar System and because of the deep Network Effect.

- Because the Dollar is the world’s reserve currency, the US enjoys the unique privilege of running a high fiscal deficit (6% of GDP)

- To cover this deficit, the US Government issues Treasury bonds, which the entire world is willing to buy.

- The interest rate on those Treasury bonds is the world’s risk-free rate.

- When the US Fed raises the interest rates (for inflation, etc., reasons), the interest rates on new bonds rise.

- Rising bond yields mean the risk-free rate will increase.

- Now, the institutional investors around the world would reduce their equity allocation by selling stocks in markets like India. The sale proceeds will now move to the US to buy high-yielding bonds.

- As a result, the stock prices in India fall.

So you can see, a decision made in a Washington meeting room ends up directly affecting the prices of stocks in your demat account.

This is the cycle.

Conclusion

- The stock market does not exist in isolation. What you see on your trading screen every morning is the result of a thousand things happening across the world.

- Learn to watch the right signals. A few things are worth tracking regularly.

- What is the US Federal Reserve doing with interest rates?

- Are US 10-year Treasury yields rising or falling?

- What is the inflation trend in the US?

- The cycle also works in reverse. When inflation cools and the Fed cuts rates, bond yields fall, equity risk premiums improve, institutional money flows back into stocks, and markets rally.

If you found this useful? Share it with one investor friend who you think would benefit from understanding the bigger picture.

Have a happy investing.