Query: Reached 2Cr at 30’s, what to do next?

Hey, I’m 30M, reached a target of 2cr portfolio mainly in equity stocks.

Been investing for the last 10 years now. I‘ve always wanted to be financially free, and I set the target of 2cr, and now that

I’m reached, I want to focus on 2 things now.

1 -> Fixed monthly income 2 -> Wealth Generation

Can you suggest to me the ways to split my 2cr rupees so that I could make me a fixed income every month + generate wealth alongside.”

Introduction

First things first, reaching a Rs. 2 crore portfolio in your 30s is not a small milestone. Congratulations.

You must have been disciplined, patient, and have carried a long-term mindset that most investors never fully develop.

However, paradoxically, reaching this type of milestone can create confusion. You are in Phase-2 of your investment journey.

Now, your question is quietly shifting from “How do I grow?” to “What exactly do I do with this now?”

The moment someone says, “I want streams of fixed monthly income,” I think it is tempting to jump straight into dividends, rental property, or income funds.

But that instinct, while understandable, can be dangerous at this age (you are young). The real challenge is not income generation alone, but designing income without suffocating future growth.

This is where financial independence needs to be reframed. It is about having the freedom to make better life choices. The freedom to say the following:

- No to a stressful job,

- To take a break if health or family needs it,

- To slow down work without worrying about monthly expenses.

- At the same time, your money should continue to grow quietly in the background for the years ahead.

Table of Contents

- Introduction

- Step One: Define Financial Independence Before Chasing Income

- Step Two: Important Understanding: 2 Crore’s Dual Purpose

- Step Three: Let One Part of the Money Do Nothing Except Grow

- Step Four: Creating Monthly Income Without Putting Future at Risk

- Step Five: How the Plan Comes Together After Retirement

- Conclusion

Step One: Define Financial Independence

These days, many talk about financial independence, but what actually is it? To understand how to define financial freedom, let’s take a hypothetical example.

Let us begin with a practical assumption.

- House Rent or Loan EMIs: In this calculation, I have not included any home loan EMIs or rent. The assumption is that the person is already living in a self-owned house, and the home loan, if any, has been fully repaid. This assumption is intentional. When the goal is financial independence, having a roof over your head that does not demand a monthly payment (Rent or EMI) is a foundational requirement. Without a loan-free home, achieving the status of true financial freedom is not possible.

- Basic Cost: Suppose your current basic monthly expense is Rs. 35,000. It covers necessities and a modest lifestyle. But financial independence cannot be designed only for survival mode. So, let’s look at another expense component.

- Comfort Cost: Let’s add a buffer for comfort. It will be occasional indulgences, travel, and unforeseen costs. I’ve considered another layer of extra cost of 60% over and above the basic expense. This will take the total monthly expense to Rs. 56,000 (35,000*(1+60%).

[Note: The Basic + Comfort costs (Rs. 56,000) have been calculated based on my estimate and observations of an average healthy retired couple in their early 60s. This is the minimum income they need per month to, as of today, to lead a decent retired life. For couples who have serious medical needs, the assumed cost will go up depending on their medical care needs.]

That translates to an annual expense requirement of approximately Rs. 6.7 lakh.

This expense number (Rs. 6.7 Lakhs) is important because it becomes the base of all future planning. If you do not know how much money you actually need every year to run your life comfortably, then the idea of “fixed income” remains vague.

To make investment decisions more accurate, which is driven more by clear financial planning, defining the total monthly expense requirement is a must.

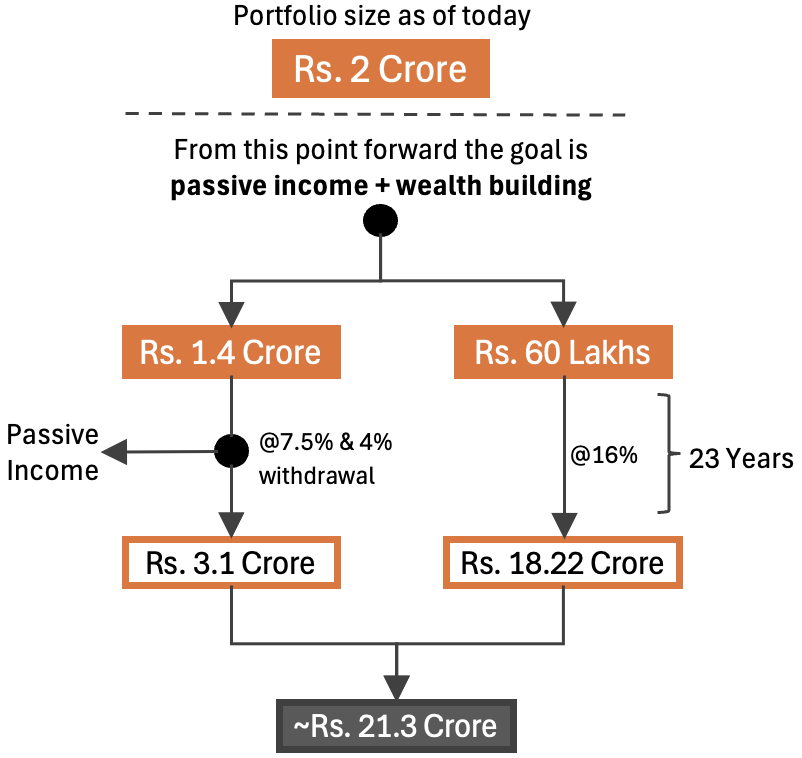

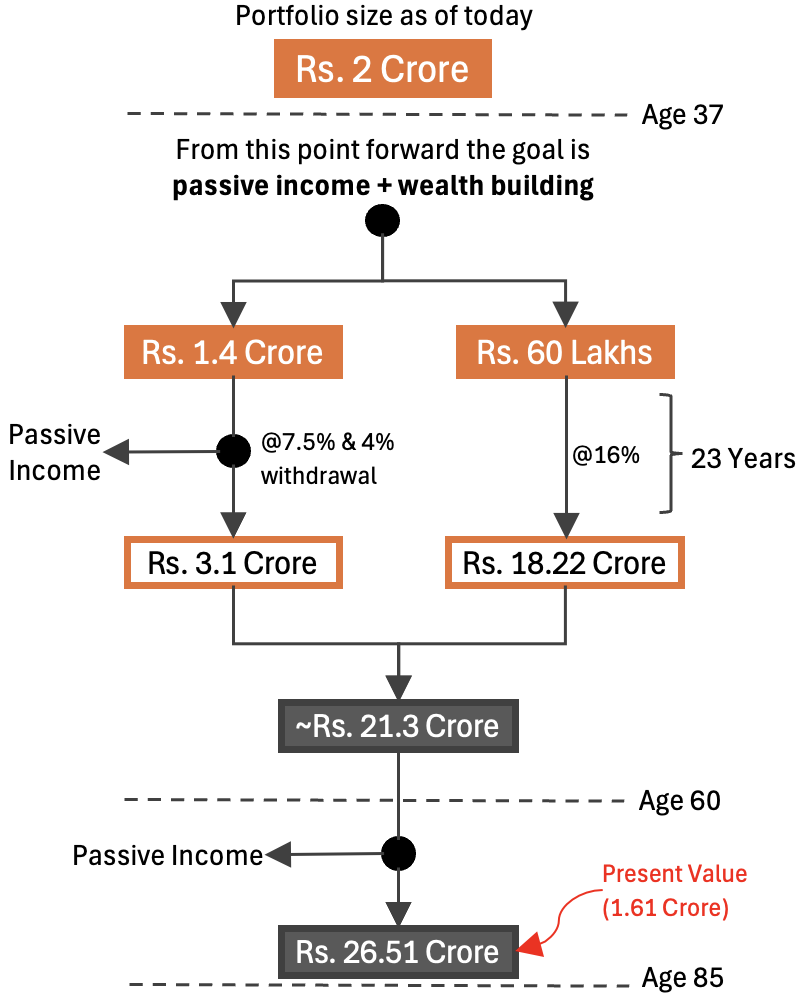

Step Two: Important Understanding: 2 Crore’s Dual Purpose

A common mistake at this stage will be to assign the entire corpus a single responsibility. Either everything must generate income, or everything must grow aggressively.

I think both approaches in isolation will be suboptimal.

Instead, the portfolio must be split based on function, not asset class:

- Financial Independence (FI) corpus (Rs. 1.4 Cr). Its only job is to provide stability and a predictable income.

- Wealth Generation corpus (Rs. 60 Lakhs): Its job will be to compound aggressively over long periods.

This separation is not cosmetic; it is intentionally created to provide the necessary psychological support.

It allows you to enjoy a steady income flow without panic during market volatility. This bifurcation also allows the capital to grow fast as it remains untouched (the power of compounding).

Step Three: Let One Part of the Money Do Nothing Except Grow

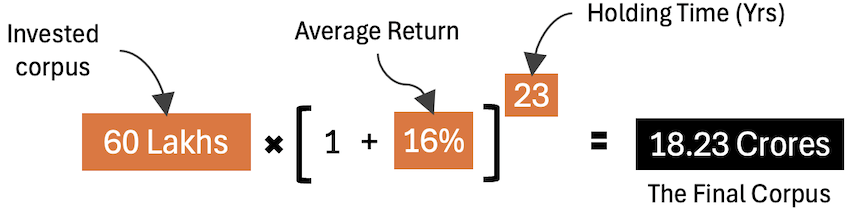

Out of the total Rs. 2 crore portfolio, Rs. 60 lakh is kept aside and left untouched. At first, this may feel uncomfortable.

When the goal is financial freedom, the natural question is, “Why not use this money to improve life today?” That question is valid. But this is exactly where long-term thinking begins.

This Rs. 60 lakh is not meant to pay monthly bills or fund vacations. It is not meant to reduce today’s stress. Its role is very simple: to stay invested and grow over time. Nothing else. It may sound boring but this is how compounding works.

Think of it as money you are locking away for your older self. You do not check it every month. You do not dip into it when markets are good or bad. You just let it remain invested, year after year.

Assuming a 16% annual return, this Rs. 60 lakh quietly grows in the background and becomes about Rs. 18 crore over the next 23 years.

The real reason this works is not the number 16%. The real reason is discipline. When money is not disturbed, time does the heavy lifting.

This part of the portfolio serves as your safety net for retirement, medical needs, and a long, comfortable life.

It is what allows the rest of your plan to work without pressure or fear.

Step Four: Creating Monthly Income Without Putting Future at Risk

Now let us talk about the remaining Rs. 1.4 crore, because this is the part of the money that most people care about the most.

This is that part of the corpus that will be used to pay the monthly bills and bring a sense of stability.

Here are a few assumptions:

- Where to invest: This amount is invested in relatively safe debt mutual funds, which will earn a return of about 7.5% per year.

- Withdrawal Rate: From this, only 4% is taken out every year for expense management. The value of 4% is carefully chosen for India as it reduces the risk of running out of money over time.

In the first year, this works out to about Rs. 5.6 lakh annually, or roughly Rs. 46,600 per month (Rs. 1.4 Crore, at 4% withdrawal rate)

But this is where we must also face the uncomfortable part. Even after having the Rs. 1.4 crore in the kitty, it seems insufficient to support even the humble expense assumption of Rs. 56,000 per month.

The passive income falls short by around Rs. 9,000 per month.

For many people, this is the moment when doubt creeps in. “If even ₹2 crore cannot fully take care of expenses, then what is the point?”

But this is where perspective matters the most.

Financial independence is not about switching off your salary in one shot. It is about slowly reducing how much you depend on it. In this setup, the job is still there, but its role is very different. It is no longer carrying the full burden of your lifestyle. It is only supporting a small gap that still remains between your ultimate goal of financial independence.

As the years go by, expenses increase because of inflation. At the same time, this debt portfolio also grows, even after regular withdrawals. The monthly income from it keeps increasing in rupee terms. The job income quietly takes care of the remaining difference, without pressure.

Imagine yourself doing a job for the next 23 years without feeling the financial burden. You have your capital (Rs. 60 Lakhs + Rs 1.4 Crore) working for you. Your working efficiency and clarity would be 2x that of your colleagues.

By the time retirement arrives, this income-focused corpus itself grows to a little over Rs. 3 crore. It is not much, but it has already served its real purpose for over two decades. It has given stability, reduced stress, and allowed the equity portion of the portfolio to grow without being disturbed.

Calculation (Today Till Retirement)

| Year | Investment | Return / Year (@7.5%) | Withdrawal @ 4% | Withdrawal / month | Expense Requirement @ 6% Inflation | Deficit From Job | Independence % |

|---|---|---|---|---|---|---|---|

| 1 | 1,40,00,000 | 10,50,000 | 5,60,000 | 46,667 | 56,000 | 9,333 | 83% |

| 2 | 1,44,90,000 | 10,86,750 | 5,79,600 | 48,300 | 59,360 | 11,060 | 81% |

| 3 | 1,49,97,150 | 11,24,786 | 5,99,886 | 49,991 | 62,922 | 12,931 | 79% |

| 4 | 1,55,22,050 | 11,64,154 | 6,20,882 | 51,740 | 66,697 | 14,957 | 78% |

| 5 | 1,60,65,322 | 12,04,899 | 6,42,613 | 53,551 | 70,699 | 17,148 | 76% |

| 6 | 1,66,27,608 | 12,47,071 | 6,65,104 | 55,425 | 74,941 | 19,515 | 74% |

| 7 | 1,72,09,575 | 12,90,718 | 6,88,383 | 57,365 | 79,437 | 22,072 | 72% |

| 8 | 1,78,11,910 | 13,35,893 | 7,12,476 | 59,373 | 84,203 | 24,830 | 71% |

| 9 | 1,84,35,327 | 13,82,649 | 7,37,413 | 61,451 | 89,255 | 27,804 | 69% |

| 10 | 1,90,80,563 | 14,31,042 | 7,63,223 | 63,602 | 94,611 | 31,009 | 67% |

| 11 | 1,97,48,383 | 14,81,129 | 7,89,935 | 65,828 | 1,00,287 | 34,460 | 66% |

| 12 | 2,04,39,576 | 15,32,968 | 8,17,583 | 68,132 | 1,06,305 | 38,173 | 64% |

| 13 | 2,11,54,961 | 15,86,622 | 8,46,198 | 70,517 | 1,12,683 | 42,166 | 63% |

| 14 | 2,18,95,385 | 16,42,154 | 8,75,815 | 72,985 | 1,19,444 | 46,459 | 61% |

| 15 | 2,26,61,723 | 16,99,629 | 9,06,469 | 75,539 | 1,26,611 | 51,072 | 60% |

| 16 | 2,34,54,884 | 17,59,116 | 9,38,195 | 78,183 | 1,34,207 | 56,024 | 58% |

| 17 | 2,42,75,805 | 18,20,685 | 9,71,032 | 80,919 | 1,42,260 | 61,340 | 57% |

| 18 | 2,51,25,458 | 18,84,409 | 10,05,018 | 83,752 | 1,50,795 | 67,044 | 56% |

| 19 | 2,60,04,849 | 19,50,364 | 10,40,194 | 86,683 | 1,59,843 | 73,160 | 54% |

| 20 | 2,69,15,018 | 20,18,626 | 10,76,601 | 89,717 | 1,69,434 | 79,717 | 53% |

| 21 | 2,78,57,044 | 20,89,278 | 11,14,282 | 92,857 | 1,79,600 | 86,743 | 52% |

| 22 | 2,88,32,041 | 21,62,403 | 11,53,282 | 96,107 | 1,90,376 | 94,269 | 50% |

| 23 | 2,98,41,162 | 22,38,087 | 11,93,646 | 99,471 | 2,01,798 | 1,02,328 | 49% |

Step Five: How the Plan Comes Together After Retirement

Retirement (Age 60) is the point where all earlier decisions start to show their real value.

- By the time retirement begins, the equity portfolio (Rs. 60 Lakhs) that was left untouched for 23 years has grown to around Rs. 18 crore.

- Along with this, the income-focused corpus has also grown to a little over Rs. 3 crore.

- Together, they form a total retirement corpus of roughly Rs. 21 crore.

At this stage, the approach should become more conservative.

At this stage (post-retirement), the objective is no longer aggressive growth. It is stability and a steady income.

This combined amount is assumed to grow at about 6% per year, which is reasonable for a low-risk retirement portfolio.

Withdrawal Rule

Withdrawals also must start carefully.

- Rate: In the first year of retirement, at age 61, only 1.5% of the corpus is withdrawn. This small takeout is intentional. Expenses in the early years of retirement are usually manageable, and there is no need to rush withdrawals. The purpose is to do everything so that the portfolio never dries out.

- Growth: Every year, the withdrawal rate increases slightly, by 0.3%, to reflect the reality that costs tend to go up as we grow older. The costs related to travel, health, and comfort go up with age.

Expenses

In the first year after retirement, the estimated monthly expense comes to around Rs. 2.16 lakh. The portfolio, however, generates close to Rs. 2.66 lakh per month (at 1.5% withdrawal rate).

For the first time in this entire journey that we’ve seen, the income from investments is comfortably higher than what is required. This excess is not a coincidence. It is the result of keeping withdrawals low during working years and allowing money to compound without disturbance.

As the years pass, expenses rise faster, and withdrawals become larger. I’ve assumed the inflation to start at 7% and gradually increase (@0.25% per annum). This way, it reflects real-life medical and lifestyle costs in later years. Even with these assumptions, the portfolio continues to hold its ground (reasonably).

- By age 85:

- The withdrawal rate reaches about 8.7%.

- Annual withdrawals are around Rs. 2.37 crore (close to Rs. 20 lakh per month).

- At this point, even the expense inflation rate becomes 13% (based on our estimate of 0.25% growth from the base rate of 7%).

- Even then, the portfolio value remains above Rs. 26.51 crore.

- In today’s terms, the present value of Rs. 26.51 crore is equivalent to Rs. 1.61 Crore.

At that stage, the concern is no longer about running out of money. The focus shifts to quality of life. And that is exactly what a well-structured retirement plan is supposed to deliver.

Calculation (From Age 60 To 85)

| Age | Corpus Size | Return / Year (@6%) | Withdrawal Rate | Withdrawal / month (Rs.) | Expense Inflation | Requirement / mon (+ Inflation) |

|---|---|---|---|---|---|---|

| 61 | 21,31,42,932 | 1,27,88,576 | 1.500% | 2,66,429 | 7.00% | 2,15,924 |

| 62 | 22,27,34,364 | 1,33,64,062 | 1.800% | 3,34,102 | 7.25% | 2,31,578 |

| 63 | 23,20,89,207 | 1,39,25,352 | 2.100% | 4,06,156 | 7.50% | 2,48,947 |

| 64 | 24,11,40,687 | 1,44,68,441 | 2.400% | 4,82,281 | 7.75% | 2,68,240 |

| 65 | 24,98,21,751 | 1,49,89,305 | 2.700% | 5,62,099 | 8.00% | 2,89,699 |

| 66 | 25,80,65,869 | 1,54,83,952 | 3.000% | 6,45,165 | 8.25% | 3,13,600 |

| 67 | 26,58,07,845 | 1,59,48,471 | 3.300% | 7,30,972 | 8.50% | 3,40,256 |

| 68 | 27,29,84,657 | 1,63,79,079 | 3.600% | 8,18,954 | 8.75% | 3,70,028 |

| 69 | 27,95,36,289 | 1,67,72,177 | 3.900% | 9,08,493 | 9.00% | 4,03,330 |

| 70 | 28,54,06,551 | 1,71,24,393 | 4.200% | 9,98,923 | 9.25% | 4,40,639 |

| 71 | 29,05,43,869 | 1,74,32,632 | 4.500% | 10,89,540 | 9.50% | 4,82,499 |

| 72 | 29,49,02,027 | 1,76,94,122 | 4.800% | 11,79,608 | 9.75% | 5,29,543 |

| 73 | 29,84,40,851 | 1,79,06,451 | 5.100% | 12,68,374 | 10.00% | 5,82,497 |

| 74 | 30,11,26,819 | 1,80,67,609 | 5.400% | 13,55,071 | 10.25% | 6,42,203 |

| 75 | 30,29,33,580 | 1,81,76,015 | 5.700% | 14,38,935 | 10.50% | 7,09,634 |

| 76 | 30,38,42,380 | 1,82,30,543 | 6.000% | 15,19,212 | 10.75% | 7,85,920 |

| 77 | 30,38,42,380 | 1,82,30,543 | 6.300% | 15,95,172 | 11.00% | 8,72,371 |

| 78 | 30,29,30,853 | 1,81,75,851 | 6.600% | 16,66,120 | 11.25% | 9,70,513 |

| 79 | 30,11,13,268 | 1,80,66,796 | 6.900% | 17,31,401 | 11.50% | 10,82,122 |

| 80 | 29,84,03,249 | 1,79,04,195 | 7.200% | 17,90,419 | 11.75% | 12,09,272 |

| 81 | 29,48,22,410 | 1,76,89,345 | 7.500% | 18,42,640 | 12.00% | 13,54,384 |

| 82 | 29,04,00,074 | 1,74,24,004 | 7.800% | 18,87,600 | 12.25% | 15,20,296 |

| 83 | 28,51,72,872 | 1,71,10,372 | 8.100% | 19,24,917 | 12.50% | 17,10,333 |

| 84 | 27,91,84,242 | 1,67,51,055 | 8.400% | 19,54,290 | 12.75% | 19,28,401 |

| 85 | 27,24,83,820 | 1,63,49,029 | 8.700% | 19,75,508 | 13.00% | 21,79,093 |

Conclusion

Reaching Rs. 2 crore in your 30s is not a signal to stop thinking about money. There is still a long way to go.

At this stage (Age 37), start thinking more clearly about what money is meant to do at different stages of life.

This entire approach shows that financial independence does not come from trying to make every rupee work equally hard all the time. It comes from giving different parts of your money different responsibilities.

- Some money is meant to support your present life.

- Some is meant to quietly grow for the future.

- And some is meant to protect you when age reduces your earning ability.

What makes this structure work is not optimism about returns, but restraint.

- Restraint in withdrawals.

- Restraint in disturbing long-term investments.

- And restraint in expecting instant freedom.

The freedom here is gradual, practical, and absolutely sustainable.

When someone manages to build a decent amount of money early in life, the real success is not about retiring as soon as possible. It is about reaching a stage where you are not forced to work just to pay bills.

You can continue working if you want to, slow down if you need to, or change direction without fear. When money gives you this flexibility, instead of controlling your choices, that is when financial independence actually makes sense over the long run.

Have a happy investing.

![What's India’s Google Tax [Explained] - Thumbnail](https://getmoneyrich.com/wp-content/uploads/2025/03/Whats-Indias-Google-Tax-Explained-Thumbnail-300x181.png)