Introduction

Recently, I got a message from one of my subscribers. He wanted me to calculate the return on investment (ROI) of an investment plan that he was considering.

Let me explain what his investment plans were, and then I will show you how I calculated the return on investment for each option.

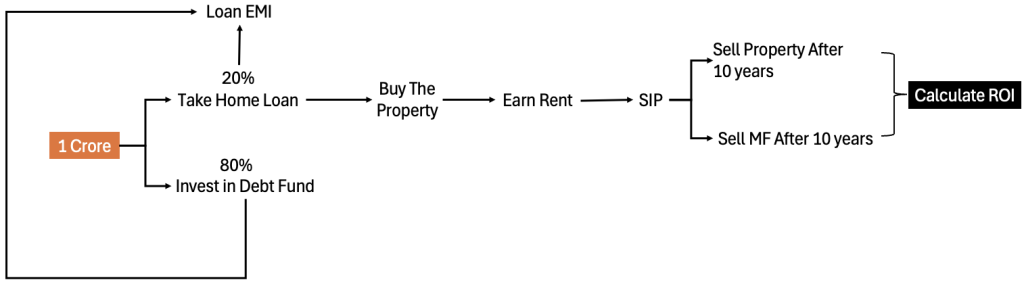

The person has Rs. 1 crore available for investing, and he wants to invest that money in a real estate property only. He was quite fixated on that investment plan for some reason.

Plan #1: His first idea was to use his Rs. 1 crore fund to buy a property and then put that property on rent. Whatever rental income he earned, he would use that money to start a mutual fund SIP. The SIP would continue for the next 10 years. After 10 years, he would sell the property and also liquidate all the mutual fund units that he had accumulated. He wanted me to calculate the ROI of this plan.

He also had another investment plan in mind.

Plan #2: Instead of using the full Rs. 1 crore to buy the property, he wanted to put only 20% as a down payment and use a home loan for the remaining amount. In this case, he would again buy the property, put it on rent, and use the rental income to gradually accumulate mutual fund units. After 10 years, he would sell the property and liquidate all the mutual fund units that he had accumulated.

So these were the two alternatives he wanted to compare. He wanted to know which plan would have a higher ROI and then take his investment decision based on that result.

In this article, I will show you how I calculated the ROI for both investment plans and present my independent conclusion, which was also kind of surprising for me. Why?

Because the higher ROI option was actually making less money. How? See for yourself.

Option #1: Self-Funded Property Purchase

To calculate the return on investment, it was important to forecast the cash flows. So let me explain the assumptions I made.

The person has Rs. 1 crore available for investing. In Option #1, he uses the entire Rs. 1 crore to buy the property. There is no home loan involved.

That is why I call it a self-funded investment.

He purchases a property worth Rs. 1 crore and earns a rental yield of 3%.

A 3% rental yield on a Rs. 1 crore property means annual rental income of approximately Rs. 3 lakh, which comes to around Rs. 25,000 per month.

I then assumed three types of costs:

- Property Tax: I assumed property tax would be around 35% of the rental income.

- Annual Maintenance Cost: For upkeep of the property, including painting, repairs, and miscellaneous maintenance work, I assumed an annual cost equal to 20% of the rental income.

- Society Maintenance Charges: I assumed society charges would be around 10% of the monthly rental income and would be paid monthly.

After adjusting for all these costs, whatever net rental income remains is invested in a mutual fund SIP.

For the SIP, I assumed an annual return of 16%. The SIP continues for 10 years. I also assumed that the property appreciates at 6.5% per annum.

Under these assumptions:

- The Rs. 1 crore property grows to approximately Rs. 1.87 crore after 10 years.

- The SIP corpus grows to approximately Rs. 88.47 lakh.

Therefore, after 10 years, the total investment portfolio becomes:

- Property value: Rs. 1.87 crore

- Mutual fund corpus: Rs. 88.47 lakh

- Total value: approximately Rs. 2.76 crore

Cash Flow Assumptions

For the purpose of calculating ROI, I assumed these cash flows:

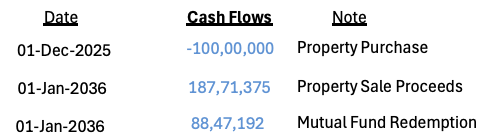

- On 1 December 2025, the investor spends Rs. 1 crore to purchase the property.

- On 1 January 2036, he received the sale proceeds of the property.

- On 1 January 2036, he also liquidates the mutual fund corpus worth Rs. 88.47 lakh.

The property purchase is a negative cash flow, while the property sale and mutual fund liquidation are positive cash flows.

Using these cash flows, I calculated the ROI using the XIRR formula available in Excel and Google Sheets.

The result came out to: XIRR = 10.56% per annum

So in the self-funded option, the investor ends up with approximately Rs. 2.76 crore after 10 years, and the annualized return works out to 10.56%.

Option #2: Buying the Property Through a Home Loan

Now let’s move to Option #2. This option is a little more complicated.

The person again has Rs. 1 crore available.

However, instead of investing the entire amount in the property, he divides the corpus into two parts.

- 20%: First, he uses Rs. 20 lakh as the down payment.

- 80%: For the remaining Rs. 80 lakh, he takes a home loan.

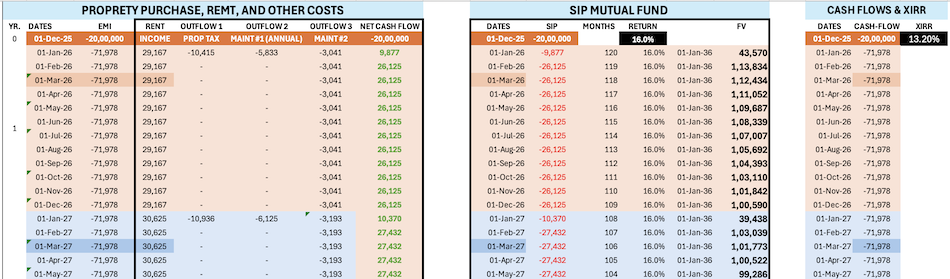

I assumed the following for the home loan:

- Loan amount: Rs. 80 lakh

- Interest rate: 9% per annum

- Loan tenure: 20 years

Using the home loan, he buys the same Rs. 1 crore property.

Again, I assumed a rental yield of 3%. In this case, there are four major costs:

- Home Loan EMI: For an Rs. 80 lakh loan at 9% interest for 20 years, the EMI comes to approximately Rs. 71,978 per month.

- Property Tax: This is again 35% of rental income.

- Annual Maintenance Cost: As before, this is also 20% of rental income.

- Society Maintenance Charges: 10% of rental income.

After paying these expenses, the remaining rental income is invested into a mutual fund SIP earning 16% annually.

But I think you must be wondering, how come even after paying the loan EMI, there is money left for SIP Investment? This is happening because of the balance of Rs. 80 Lakhs in the investors’ kitty.

What Happens to the Remaining Rs. 80 Lakh?

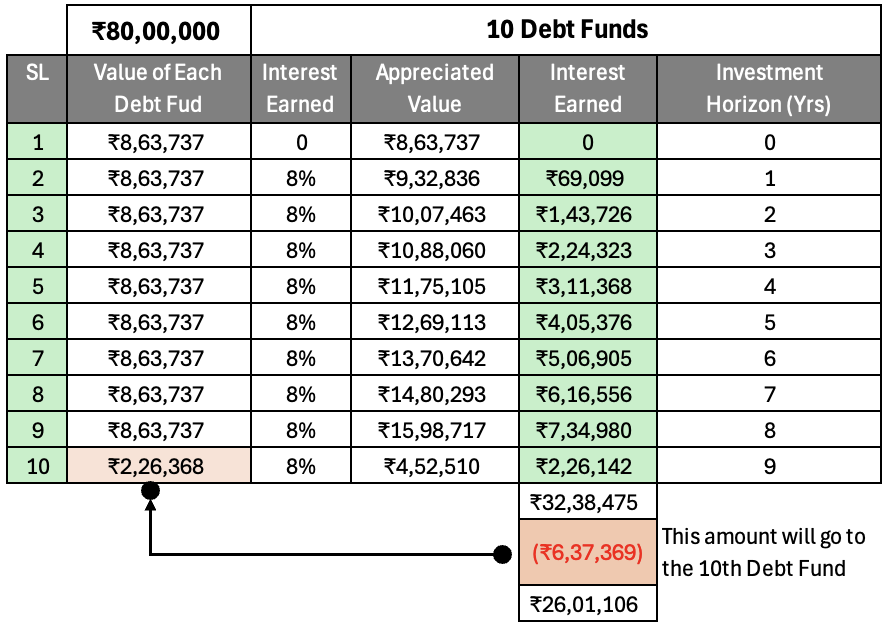

Since only Rs. 20 lakh is used as the down payment, the remaining Rs. 80 lakh is invested in a debt fund.

To simplify the planning, I assumed that this Rs. 80 lakh is divided into ten separate buckets.

The logic is simple.

The annual EMI outflow is approximately Rs. 8,63,737 (Rs. 71,978 x 12).

Therefore, I assumed nine debt-fund buckets of approximately Rs. 8,63,737 each and one bucket of Rs. 2,26,368. The sum of all these bickets is Rs. 80 Lakhs.

Whenever the investor needs money to pay the home loan EMI, he redeems units from the corresponding debt-fund bucket.

- I assumed that the debt fund earns 8% per annum.

- For the first year, I assumed a 0% return because the money remains in a savings account.

- From the second year onwards, the debt fund earns 8%.

Some buckets remain invested for one year, some for two years, some for three years, and so on, up to nine years.

When all calculations are completed, the total interest earned from the debt fund over the 10 years comes to approximately Rs. 32.38 lakh.

Out of this amount, around Rs. 6.37 lakh is required to complete the final debt-fund bucket (2,26,368 + 6,37,639 = 8,63,737).

What will be remaining in the debt fund bucket will be approximately Rs. 26 lakh (after paying all the EMI for 10 years). This becomes the additional cash available to the investor.

Meanwhile, the rental income continues to fund the mutual fund SIP, which compounds at 16% annually.

Let’s see what the position is after 10 Years:

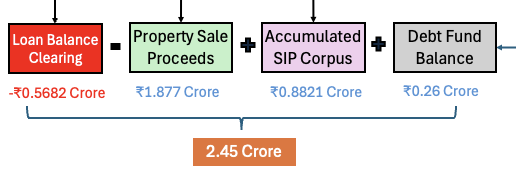

- Property Value: The property appreciates from Rs. 1 crore to approximately Rs. 1.87 crore.

- Outstanding Loan: After 10 years, the remaining loan balance is approximately Rs. 56 lakh. Therefore, before selling the property, the investor repays the outstanding loan balance of Rs. 56 lakh.

- Mutual Fund Corpus: The SIP grows to approximately Rs. 88 lakh.

- Debt Fund Balance: The investor also receives approximately Rs. 26 lakh from the debt-fund strategy.

Therefore, the final cash flows include:

- Property sale proceeds

- Less outstanding loan repayment

- Debt fund proceeds

- Mutual fund corpus

XIRR Calculation For Plan 2

For this investment plan, the cash flows include:

- Initial down payment of Rs. 20 lakh

- Monthly EMI payments (Rs. 71,978 each for 10×12 months)

- Final inflows from property sale, debt fund proceeds, and mutual fund corpus

Using the XIRR formula in Excel or Google Sheets, I calculated the return on investment.

The result came out to: XIRR = 13.2% per annum

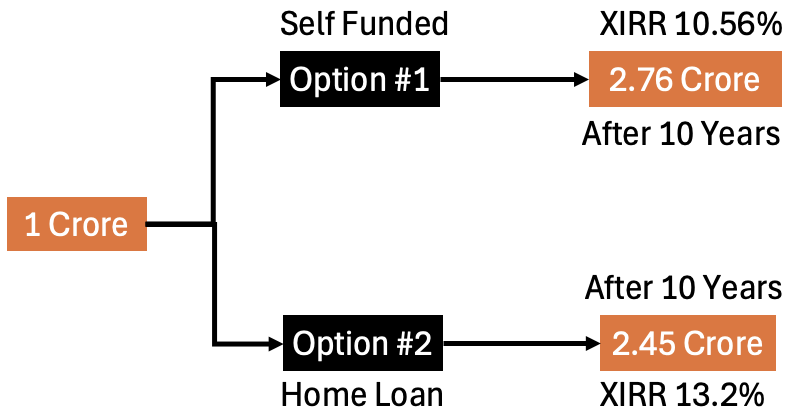

Conclusion

You can see that the home-loan-based investment plan generates an XIRR of 13.2%, while the self-funded plan generates an XIRR of 10.56%.

However, there is something very important to note here.

In the self-funded option, the investor ends up with approximately Rs. 2.76 crore after 10 years.

In the home-loan option, the investor ends up with approximately Rs. 2.45 crore.

So even though the XIRR appears higher in the home-loan strategy, the actual amount of money in the investor’s pocket is lower.

In other words:

- Option #1: Final value ≈ Rs. 2.76 crore, XIRR = 10.56%

- Option #2: Final value ≈ Rs. 2.45 crore, XIRR = 13.2%

This is why I think the investor should not make the decision based only on ROI.

He should also look at the actual cash flows and the final amount of money that he will have at the end of the investment period.

For this particular case, Option #1 generates more wealth in absolute terms.

That is why I think the self-funded route is the better option for this investor.

I hope you found this analysis useful.

Consider subscribing to my blog on YouTube, WhatsApp, Telegram, and Substack. You can also follow me on Twitter (X).

Have a happy investing.