Introduction

Would you agree with this fact or not that we, stock investors, are almost trained to admire growth? For example, a company growing its net profit or EPS at a rate of 15-20% per annum is immediately seen as superior to one growing at 8-10%.

I think, right at this time, when you are reading my post, you are almost thinking, why am I questioning whether 20% is better than 10% or not? It is simple mathematics, right?

But when it comes to stock analysis, this mathematically obvious conclusion is not always correct.

Most of our screeners are built around the same growth rate numbers – the higher the better.

Even the management and investor presentations highlight CAGR charts. Analysts debate whether growth will be 18% or 22%.

But there is a far more important question that needs to be asked before we can conclude whether the reported growth number is good or not.

What is the important question I’m referring to?

Is this growth actually creating value for shareholders?

Because the uncomfortable truth is that not all growth is good. In fact, for some companies, growth actually quietly destroys their value. This is true even for those companies that report growing profits year after year.

This is the reason why we must learn to distinguish between value-creating growth and value-destroying growth. Without this clarity, we may end up owning businesses that look successful on the surface but steadily erode shareholder wealth underneath.

In this post, I’ll try to highlight how we investors can identify value-destroying growth companies with the use of real-life examples.

The Illusion of All Growth is Good

I want you to consider a simple situation.

Suppose there is a company that has been growing in profits at 20% per annum for the last five years. The profit is growing along with the revenue. The business looks as if it is expanding year on year, and it looks more important and more impressive.

This is how we see companies whose revenue and profits are growing, right? This is especially true when the reported growth numbers look like 15-20% CAGR.

But it is also necessary to understand that such growth numbers by itself tells us nothing about where shareholders’ value is getting created or eroded. Why is it so?

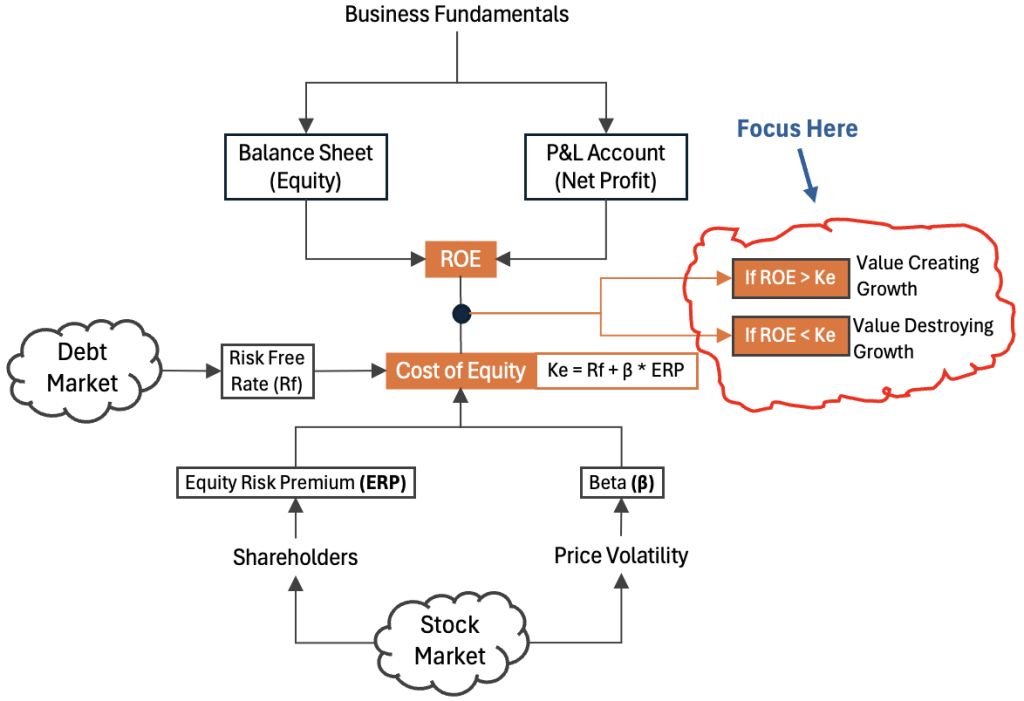

To understand this, we must know how a company grows. The key is the ability of the company to reinvest its capital. What are the ways the company practices the reinvestment process?

- Reinvestment of retained earnings

- Using capital for CAPEX

- Using working capital to manage operations

- Acquisitions of other businesses, etc.

All these steps will lead to growth, higher revenue, and profits. But what really matters is the quality of growth.

How to measure the quality of growth? By knowing what return the company earns on its reinvested capital.

But do we check this detail when analyzing our stocks? No, we simply see the revenue and profits growing, and we conclude that all is well.

This is where our analysis usually breaks down because it is incomplete.

The Growth Question That Matters More Than Growth Itself

Every growing company’s management should be answering this one question every year to all its stakeholders:

“If we retain Rs. 1 instead of paying it out to shareholders, what return is being earned on that Rs. 1?”

To answer this question, we must also ask, “What return do the shareholders require from investing in this business?” The answer to this question is the cost of equity.

Comparing the return generated by the reinvested capital with the cost of equity will give us our answer.

We’ll discuss this part in more detail using calculations for two Indian stocks: Asian Paints and Indian Oil Corporation.

Two Types of Growth [Only One Creates Value]

1 Value-Creating Growth

Growth is value-creating when ROE > Cost of Equity

In these types of companies, every rupee that is reinvested earns more than what shareholders could reasonably earn elsewhere at a comparable risk.

When retained profits compound at a good rate, which is more than the cost of equity, it also makes the intrinsic value rise faster than the company’s book value.

This is the kind of growth that quietly makes long-term shareholders wealthy.

How does intrinsic value get enhanced?

Imagine intrinsic value as the actual worth of a business. It is not the market price we see on the screens.

Intrinsic value is the present value of all the cash the business will generate for shareholders in the future. To understand this theory more clearly, read my post on the net present value concept.

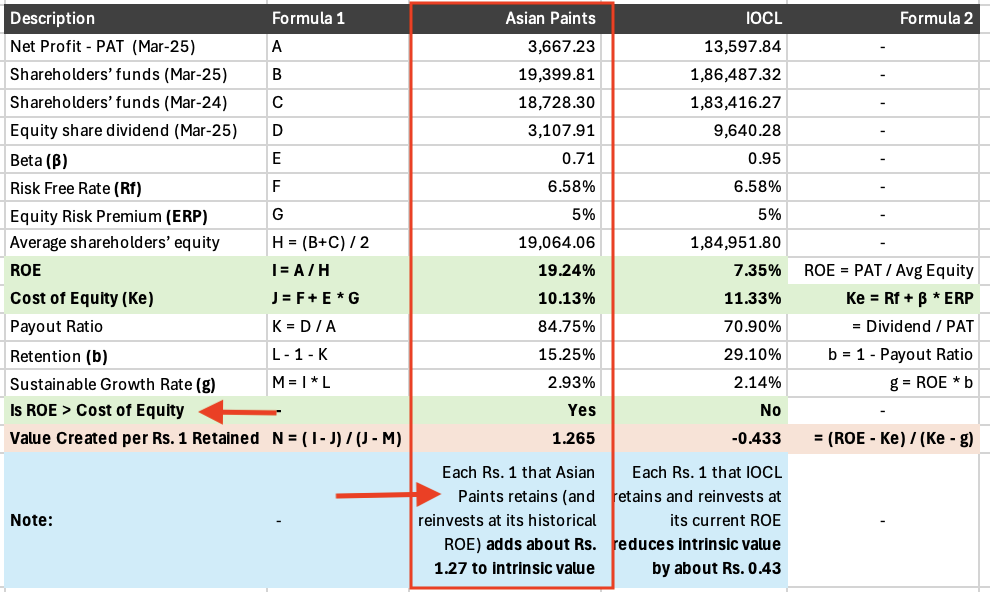

Let’s take the example of Asian Paint, which has value-creating growth.

In the above calculation table, you can see that the Asian Paints ROE is 19.24% and its calculated Cost of Equity (Ke) is 10.13%.

As ROE > Ke, we can say that Asian Paint’s growth is good for investors. How?

Because each rupee that Asian Paints retains and reinvests for growth adds value to the shareholders. The value added has also been quantified in the calculation.

Each Rs. 1 that Asian Paints retains and reinvests adds about Rs. 1.27 to its intrinsic value.

When we say “Asian Paints reinvesting at its historical ROE adds to intrinsic value,” we mean this: Asian Paints takes Rs. 1 that belongs to shareholders and uses it inside the business in a way that earns a return higher than what shareholders require for the risk they are taking.

Because that Rs. 1 now produces more cash over time than shareholders could reasonably earn elsewhere, the total future cash flows of the business increase by more than Rs. 1 in today’s terms.

That extra future cash is why intrinsic value goes up.

2. Value-Destroying Growth

Growth is value-destroying when ROE < Cost of Equity.

In these types of companies, every rupee that is reinvested earns less than what shareholders could reasonably earn elsewhere at a comparable risk.

It means the company is reinvesting shareholder money at returns below the required rate of return. Profits may still grow, sometimes rapidly, but each rupee retained is worth less than a rupee paid out.

Simple example of value-destroying growth.

Let’s understand it this way. Suppose you are a shareholder in a company, ABC. As per the net profit (PAT) reported by ABC, at a 100% payout ratio, you become eligible for a dividend of Rs. 15,000. Had you received this dividend, you could have invested this money in a Nifty Index fund, which yields a return of 11.5% per annum as per your expectation.

But instead of payinga dividend, ABC decides to retain its profit and reinvest it back into its business. If the ROE of ABC is, say, 8% per annum, it means that it is less than the return you could have potentially earned from an index fund (11.5%).

This is an example of value-destroying growth.

Such companies look busy. Even their revenues rise, and profits increase. But intrinsic value per share stagnates or even declines.

This is how investors end up owning “growing” businesses that deliver mediocre or poor long-term returns.

How does intrinsic value get depleted?

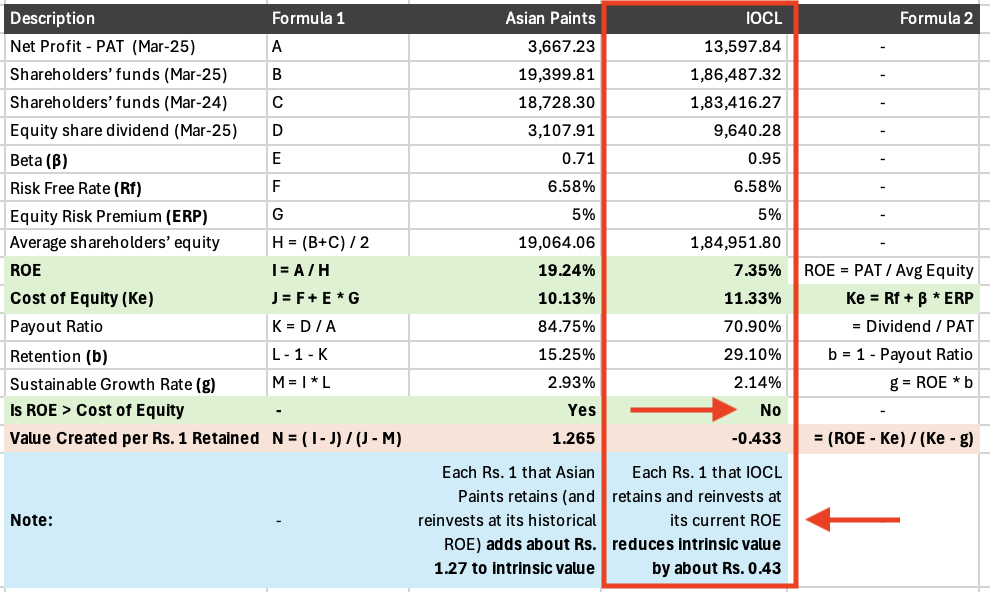

Unlike the Asian Paints example, let’s flip the situation and look at Indian Oil Corporation. In this example, we’ll see how shareholders’ value gets eroded.

In the above calculation table, you can see that the IOCL’s ROE is 7.35% and its calculated Cost of Equity (Ke) is 11.33%.

As ROE < Ke, we can say that IOCL’s growth is not good for investors if the company reinvests its profit. How?

For each Rs. 1 that IOCL retains and reinvests at its current ROE, it reduces the intrinsic value by about Rs. 0.43

When we say “IOCL reinvesting at its current ROE reduces intrinsic value,” we mean that IOCL takes Rs. 1 from shareholders and invests it at a return lower than what shareholders require.

That Rs. 1 could have earned more if it had been paid out and invested elsewhere.

As a result, the future cash flows generated by that Rs. 1 are worth less than Rs. 1 today.

Even though the profits of IOCL may still rise, the economic value created is insufficient. This shortfall is why intrinsic value declines. Please note that the growth is happening, but at the cost of shareholder wealth.

Why Headline Growth Is So Misleading

Two companies can both report 15% earnings growth.

- One is reinvesting capital at 18% ROE with a cost of equity of 11%.

- The other is reinvesting capital at 8% ROE with a cost of equity of 12%.

From a distance, they look identical, but from a valuation perspective, they are opposites.

The first company compounds value. The second company compounds disappointment.

This logic can also be used to explain the following market observations:

- Why some fast-growing companies never reward shareholders.

- Why certain “boring” businesses with modest growth create enormous wealth over time.

- Why dividend-paying companies can sometimes outperform aggressive reinvestors.

So, we must learn to observe growth with the contest of cost of capital. Without comparing long ROE and Cost of Capital, the reported growth may mean nothing.

The Decision To Retain Profits

Growth is not just a result; it is a decision.

A company chooses how much to retain and how much to distribute.

- High-ROE businesses often retain less capital because they do not need much to grow.

- Low-ROE businesses often retain more capital in an attempt to grow their way out of mediocre economics.

Ironically, the companies that should retain more often retain less, and the ones that should retain less often retain more.

Why do you think some High-ROE businesses retain less? Because they are not sure if there is a demand for it.

This is why the payout policy cannot be analyzed independently of ROE.

Once you view growth through this lens, valuation starts to make more sense.

- High growth funded at high ROE deserves a premium.

- High growth funded at low ROE deserves skepticism, not celebration.

- Low growth funded at high ROE can still be enormously valuable.

- Low growth funded at low ROE is usually a dead end.

Hence, we can say that growth does not deserve a premium by default. Only value-creating growth does.

A Practical Way to Think About Growth

When analyzing a company, try reframing the story in your head.

Instead of asking:

- How fast are earnings growing?

Ask:

- What return does the company earn on the earnings it retains?

- Is that return above or below the cost of equity?

- Would shareholders be better off receiving this money as dividends?

These questions force you to think like a business owner, not a momentum trader.

Why does this distinction matter more in today’s times?

This is a period of easy capital and optimistic narratives.

I often see value-destroying growth getting celebrated. Companies are rewarded for scale, expansion, and ambition, even when underlying returns are weak.

Conclusion

If ROE is less than Cost of Equity (Ke), the company should not reinvest its profits back into the company? Is this what we can conclude here? Yes.

If a company’s ROE is consistently lower than its cost of equity, it is better for shareholders if the company does not reinvest its profits and instead returns the money to them (through dividends or buybacks).

But we must remember that the important qualifier here is the term “consistently.”

If low ROE is temporary and expected to improve meaningfully, reinvestment may still make sense. But if ROE stays below the cost of equity, reinvesting profits destroys shareholder value.

Now, let’s ask another important question:

If the ROE is consistently lower than the cost of equity, but the company wants to grow, should such companies take the debt route to fund their growth? As the cost of debt is generally less than the cost of equity, will debt-funded growth be better or not?

In general, the answer to this question will be No. In such a case, even the use of debt to fund growth will not solve the problem if the underlying returns are weak.

If a company’s business earns returns below the cost of equity, that usually means its operating economics are poor, and adding debt only masks the issue rather than fixing it.

While the cost of debt is lower than the cost of equity, debt increases financial risk and does not change the fundamental return the business earns on its investments.

If the return on capital employed (before leverage) is below the weighted average cost of capital (WACC), using debt merely shifts risk to shareholders and lenders without creating real value.

Debt can improve ROE mechanically, but it cannot turn value-destroying growth into value-creating growth unless the underlying business returns improve.

Have a happy investing.

Please wait for my next article. You can also subscribe to my newsletters and get notifications of a new post right into your inbox.