INTRODUCTION

Today I want to discuss something that has been quietly bothering many long-term investors.

I’m talking about those types of investors who have traditionally trusted Indian IT companies as stable compounders in their portfolio

I’m not here to predict stock prices or give any buy or sell calls.

What I want to do is to take a pause from investing and understand what is structurally changing in the Indian IT industry because of AI

…and more importantly, what that means for us as investors.

Let me start with a simple observation.

If you look at the Nifty IT Index over the last few years, it touched its bottom at around mid-2022.

After that, we saw a strong price rally. It was almost 70% plus rally. It continued till late 2024.

Till 2024, everything was looking normal.

IT companies were reporting decent numbers:

- Cash flows were strong,

- Balance sheets were clean, and

- Valuations were respectable.

But then something changed around late 2024.

- This change wasn’t a recession.

- It wasn’t a financial crisis.

- It wasn’t even a collapse in demand of IT services and products.

What changed was the expectation investors had with their IT stocks, and why that happened? Because something big was happening in the background.

Around that period, the concept of Generative AI usage was no longer limited to the software engineers alone.

Suddenly everyone:

- Clients,

- Management teams,

- Media, and

- Investors

Everyone started using and understanding more deeply what AI could actually do.

And then came the next layer of innovation: Agentic AI.

This was even more important and disruptive than GENAI. Why?

Because Agentic AI was set to attack the whole business model of our IT sector.

Table of Contents

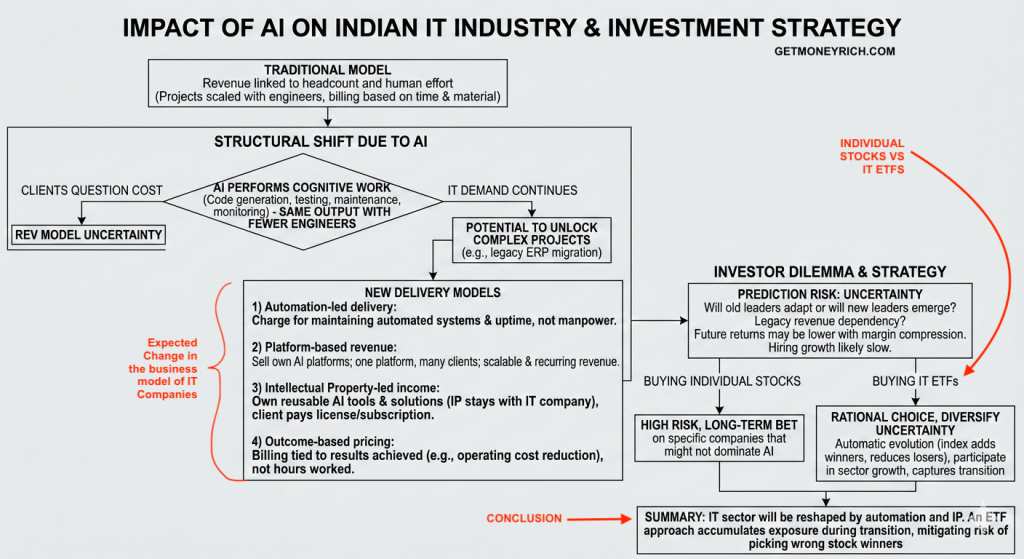

1. OLD BUSINESS MODEL OF IT COMPANIES

Traditional Indian IT companies were built on one very powerful business model, it’s called the global delivery model.

As per this model, more engineers meant more revenue for the IT companies.

Projects of our IT companies used to scale with the headcounts allotted to the project.

The billing of our IT companies was linked, directly or indirectly, to human effort.

For nearly three decades, this business model worked beautifully for Indian IT companies.

But when AI came, it introduced something fundamentally different from what our IT companies were doing.

For the first time, AI-based software can perform cognitive work like real human beings.

- It can write code,

- it can test applications,

- it can maintain systems,

- generate documentation, and

- it can also monitor the IT infrastructure.

These were the tasks that earlier required thousands of engineers, and for each engineer employed, the companies could do extra billing.

But when AI could do the same tasks, the clients started questioning:

“If AI can do all or part of this work, why should I pay for the same number of people?”

This is where the real disruption lies.

I do not think that IT demand will disappear. There will be companies that will continue to spend on technology.

In fact, technology spending may even increase because AI will enable unlocking even those projects which are considered very difficult to execute in current times (like legacy ERP migration, etc.).

But the revenue model will change for sure.

The Earlier model was:

Revenue = Number of engineers × Billing rate.

Going forward,

The way IT companies earn money is likely to change quite significantly.

Let me explain this in a way that I’ve understood it.

Until now, most Indian IT companies have operated on what we can call a people-based revenue model.

Suppose a large US bank wanted to maintain its software systems. An Indian IT company would deploy, say, 500 engineers for development, testing, maintenance, and support.

The client would then pay based on the number of people working and the number of hours billed.

So effectively, revenue depended on three things:

- How many engineers were deployed?

- For how long the project continued?

- And the billing rate per engineer.

If the company wanted to grow revenue by 10–15%, the straightforward solution was to hire more people or increase billing rates slightly.

This is why, historically, employee count and revenue growth moved almost together in Indian IT companies.

Now, AI will change this method of billing

Let’s take the example of banking.

Earlier, writing and testing software required large teams, who used to manually review the code, fix the bugs, prepare the documentation, and used to run the test cases well.

Today, AI tools can generate code, automatically can test the applications, identify errors, suggest fixes, and even monitor systems after deployment.

So instead of deploying 500 engineers, the IT company might now need only 150 engineers supported by AI systems.

From the client’s perspective, the work still gets done — possibly faster and with fewer errors.

But here’s the key question:

If fewer people are required, can the IT company still bill the client in the same way as before?

The answer is NO.

2. NEW DELIVERY MODELS

So IT companies are now shifting toward new ways of billing clients.

Here is a list of new delivery models that will function in times to come:

- Automation-led delivery

- Platform-based revenue

- Intellectual Property-led income

- Outcome-based pricing

Let me explain all of these as the way I’ve understood it till now.

(2.1) Automation-led delivery.

I think one major shift will be toward automation-led delivery.

What does this mean?

Instead of charging for manpower, companies may charge for maintaining the automated system itself.

For example, rather than billing 100 engineers for infrastructure monitoring, the IT firm could deploy an AI-driven monitoring platform and charge a fixed annual fee to keep the systems running smoothly.

The client will then pay for reliability and uptime, and not for how many people are sitting behind the screens.

(2.2) Platform-based revenue

The second revenue model can be a platform-based revenue.

Imagine an IT company that has developed its own AI platform that helps insurance companies process claims automatically.

Once built, the same platform can be sold to multiple clients.

Earlier revenue looked like this:

One project → One client → Large manpower deployment.

Now it becomes:

One platform → Many clients → Scalable and recurring revenue.

This is very different financially because revenue no longer grows linearly with employee hiring.

(2.3) Intellectual property-led income.

The third change will be intellectual property-led income (IP).

Historically, Indian IT companies mostly executed client-owned projects.

The developed software belonged to the client.

In the future, our IT companies will own the reusable AI tools,

Say, if TCS is doing the project for a US Bank, the software will now be owned by TCS, and not by the US Bank.

IT companies will develop industry-specific solutions, and they will also own the IP for these systems (not the clients)

Clients would then pay for the licensing or subscription fees to use these assets.

So instead of selling effort, our IT companies will then sell their capability.

So you can see the focus is changing. The IT companies will not be able to bill for showing that so many people are deployed on a project. The client will only pay for the end capability of the developed system. The client will not bother if one person has built the whole system or a team of 100.

(2.4) And finally, we may see more outcome-based pricing models.

For example, instead of saying, “We will provide 200 engineers,” an IT company might say, “We guarantee a 30% reduction in your operating costs if you use our AI automation.”

A major portion of the payment will depend on the result achieved and not on hours worked.

This changes the nature of cash flows completely for the IT companies.

Indian IT companies will have to transition from being large providers of skilled manpower to becoming creators and operators of technology solutions.

And this transition period is exactly where uncertainty is arising for investors who want to invest in IT stocks.

What is the uncertainty?

Not every company will move successfully from a manpower-driven model to a technology-and-IP-driven model.

I strongly feel that new leaders (companies) will emerge in the coming years who will drive the AI-led revolution in the IT sector.

3. EXCHANGE TRADED FUNDS (ETFs) vs Stocks

This shift has already started.

The only thing is, it is not visible to us now.

But I think during business negotiations, the clients must have already been demanding much sleeker projects with fewer manpower and more AI-based systems and solutions.

And this shift is why IT stocks are currently experiencing such deep corrections.

This situation is not simple for IT companies, for sure.

But I will say it is not easy for the investors as well.

There is a genuine dilemma among investors.

The question is this:

Companies like TCS, Infosys, HCLTech, Wipro, Tech Mahindra, etc are excellent organizations with strong execution history, but will they continue to lead the sector, or will new leaders emerge?

Today, the question is not about past excellence.

The question is: Who adapts best to an AI-driven world?

And honestly — nobody knows yet.

Some companies may successfully move toward AI-led solutions

Some may struggle because their legacy revenue still depends heavily on large workforce deployment.

If we look back into history, it will tell us something very important here.

Whenever a major technological shift happens — whether it was industrialization, personal computers, the internet, mobile phones, or cloud computing- industries have always survived, but leadership changes.

Old leaders don’t always disappear, but new leaders almost always emerge.

So, as investors, we are facing a prediction risk.

If we buy one or two IT stocks today, we are essentially making a long-term bet on a few stocks that are now considered good.

And this brings us to this core question.

In such a situation, does it make more sense to own individual IT stocks… or must we invest in the whole IT sector through an investment product like Nifty IT ETFs?

Personally, when an industry is undergoing such a huge structural change, I find sector exposure more rational than such concentrated bets on individual stocks.

Why?

Because an index automatically evolves.

If some companies fail to adapt, their weight reduces over time, or they will be removed from the index.

If new AI-era winners emerge, they will eventually be added to the index.

Old companies will go, and new companies will enter. The Index will continue to grow and evolve. Till the industry is alive and growing, the index too will keep its momentum.

And this is where I like ETFs more than individual stocks, especially in an industry like IT, which is seeing a radical shift.

The ETF will quietly capture the transition without requiring us to constantly predict winners and losers.

In other words, instead of betting on who survives, by investing through ETFs, we are just participating in whatever survives.

That said, I think we must also remain very realistic.

4. FUTURE RETURN PROSPECTS

The IT sector may not deliver the same smooth compounding it gave between 2005 and 2024.

Productivity gains from AI can initially compress the revenues in the coming couple of years.

Why?

Because the same amount of client work will now require significantly fewer engineers. This in turn would reduce the billable manpower under our traditional contracts.

The Hiring growth will also slow down.

Why?

Because companies will rely more on AI automation instead of expanding their employee headcount.

Now, to scale projects, they will not need more people but more AI automation.

To develop these systems, they will hire people, but it will not be in the same volume as before.

As a result, in the next 2-3 years, the valuation multiples of IT Stocks may remain under pressure during this transition phase.

This will happen because investors generally assign lower premiums to those stocks or industries that are facing uncertainty.

As the whole business model of these IT companies is going to change, and in their initial stages, their margins will also compress.

These types of uncertainties surely lead to lower valuations for stocks.

So, if I have to maintain my exposure in IT companies, I would rather do it via an IT ETF and will not buy direct stocks.

This will be my way of diversifying uncertainty and still maintaining my exposure in the IT sector.

Historically, my exposure to Software companies was about 3-4%. I’ll continue to maintain the same exposure, but now, it will be through ETFs.

AI is unlikely going to kill the IT industry. But it will almost certainly reshape it.

- Ten or fifteen years from now, Indian technology companies may look very different. There will be fewer people working per dollar of revenue.

- There will be more automation and more IP ownership.

- And I believe that an entirely new set of leaders may emerge in the IT sector due to the AI effect.

At this time, maybe these changes are not so visible because today we are standing inside this transition.

But slowly, we’ll begin to see this structural change in the IT sector.

So for an investor like me, who wants to invest in India’s technology sector but is unsure about which company will dominate the AI era, a Nifty IT ETF becomes a logical approach.

At this stage, where the IT index only looks to be in the correction mode, gradual accumulation of ETF sound a fair idea.

Remember, we are doing this not because stock picking is wrong, but I think traditional IT companies may go away, and new leaders will emerge.

So in this case, making a pointed bet on a few stocks sounds too risky.

I want to participate in this structural change going on in the IT sector, but I’m no longer sure which stock will perform.

In such a situation, I’ll prefer investing through an ETF and not directly in stocks.

List of IT stocks that look good:

| SL | Name | Price | Market Cap (Cr) | Price (52W Low) | Price from 52W Low (%) | Remarks |

| 1 | TCS | 2,557.60 | 9,25,380.15 | 2,546.40 | 0.44 | The biggest IT stock is trading very close to 52W low |

| 2 | INFY | 1,308.40 | 5,30,546.54 | 1,264.10 | 3.39 | The biggest IT stock is trading very close to 52W low |

| 3 | HCLTECH | 1,356.70 | 3,68,203.65 | 1,302.75 | 3.98 | The biggest IT stock is trading very close to 52W low |

| 4 | LTIM | 4,292.00 | 1,27,194.15 | 3,802.00 | 11.42 | – |

| 5 | COFORGE | 1,162.90 | 39,030.06 | 1,129.70 | 2.85 | High growth IT stock trading close to 52W low |

| 6 | LTTS | 3,187.40 | 33,778.84 | 3,140.00 | 1.49 | Very close to 52W Low |

| 7 | KPITTECH | 698.55 | 19,154.43 | 695.40 | 0.45 | Very close to 52W Low |

| 8 | ECLERX | 3,021.80 | 14,396.84 | 2,168.00 | 28.25 | |

| 9 | FRACTAL | 798.40 | 13,724.54 | 733.70 | 8.10 | Very close to 52W Low |

| 10 | BLS | 255.85 | 10,542.63 | 245.95 | 3.87 | Very close to 52W Low |

| 11 | BSOFT | 371.20 | 10,401.83 | 331.00 | 10.83 | – |