Q: I took a Rs. 50,00,000 home loan for 20 years at 8% interest, and the bank says my EMI is about Rs. 41,800.

They also keep telling me it’s a ‘reducing balance loan,’ but I don’t really get that.

In the first month, they say almost Rs. 33,000 out of my EMI is just interest and only around Rs. 8,800 goes toward the principal. Later, the interest part will reduce and the principal part will increase.

But why isn’t the interest simply 8% of the Rs. 50,00,000 I borrowed?

And if I prepay, say Rs. 5,00,000 after a few years, will that actually save me a lot of interest?

Basically, how is this reducing balance loan interest really being calculated?

Answer:

When you took your Rs. 50,00,000 home loan at 8% interest for 20 years, the bank told you it’s a “reducing balance loan.” That term sounds fancy, but it’s actually pretty straightforward.

Unlike a fixed interest loan (where the interest is calculated on the full loan amount for the entire term), a reducing balance loan calculates interest only on the outstanding loan amount each month.

As you pay your EMI, Rs. 41,800 in your case, part of it reduces the principal, so the next month’s interest is calculated on a slightly smaller amount.

This is why the interest portion of your EMI starts high (Rs. 33,000) and gradually decreases, while the principal portion increases over time.

Quick Analogy

Let’s dive into a more detailed analogy to really drive home how a reducing balance loan works compared to a fixed interest loan.

Imagine you borrow Rs. 1,000 from a friend to buy a phone. You’ll pay it back over 10 months with 10% annual interest.

Your friend offers two ways to calculate interest:

- Fixed Interest: You pay interest on the full Rs. 1,000 every month, even as you pay back the loan. So, the interest is always Rs. 1,000 × 10% ÷ 12 = Rs. 8.33 per month.

- Reducing Balance: You only pay interest on what you still owe.

- In month one, interest is Rs. 8.33 (10% of Rs. 1,000). If you pay Rs. 100, Rs. 8.33 covers interest, and Rs. 91.67 reduces the loan to Rs. 908.33.

- Second month, interest is lower (10% of Rs. 908.33 ≈ Rs. 7.57), so more of your payment goes to the principal.

This way you can see, it saves you money as interest shrinks each month.

Your home loan is like this reducing balance deal. Each EMI reduces what you owe, so the interest (like the Rs. 33,000 in your first EMI) gets smaller over time, unlike a fixed interest loan where it stays the same.

Why Isn’t the Interest Just 8% of Rs. 50,00,000?

You’re probably thinking: “8% of Rs. 50,00,000 is Rs. 4,00,000 per year, so shouldn’t my monthly interest be Rs. 4,00,000 ÷ 12 = Rs. 33,333?” That’s a logical assumption, but it’s not how reducing balance loans work. Let’s dig into the math to see why your first month’s interest is around Rs. 33,000.

Your EMI of Rs. 41,800 is calculated using a formula that ensures the loan (principal + interest) is fully paid off in 20 years (240 months). The formula (often computed in Excel using the PMT function) balances the principal repayment and interest so that each EMI is the same, but the split between interest and principal changes over time.

In the first month, your outstanding loan is the full Rs. 50,00,000. The interest for that month is:Interest = (Outstanding Principal × Annual Interest Rate) ÷ 12= (50,00,000 × 8%) ÷ 12 = Rs. 33,333

This is close to the Rs. 33,000 the bank mentioned. The slight difference might be due to rounding or specific terms in your loan agreement. So, your EMI of Rs. 41,800 breaks down as:

- Interest: ~Rs. 33,000

- Principal: Rs. 41,800 − Rs. 33,000 = ~Rs. 8,800

After paying this EMI, your outstanding loan drops to Rs. 50,00,000 − Rs. 8,800 = Rs. 49,91,200. In the second month, the interest is calculated on this new, slightly lower amount:

Interest = (49,91,200 × 8%) ÷ 12 ≈ Rs. 33,274

Notice how the interest is a bit less because the principal is lower. This cycle continues, with the interest portion shrinking and the principal portion growing each month. That’s the magic of a reducing balance loan—it saves you money over time compared to a fixed interest loan, where the interest stays constant.

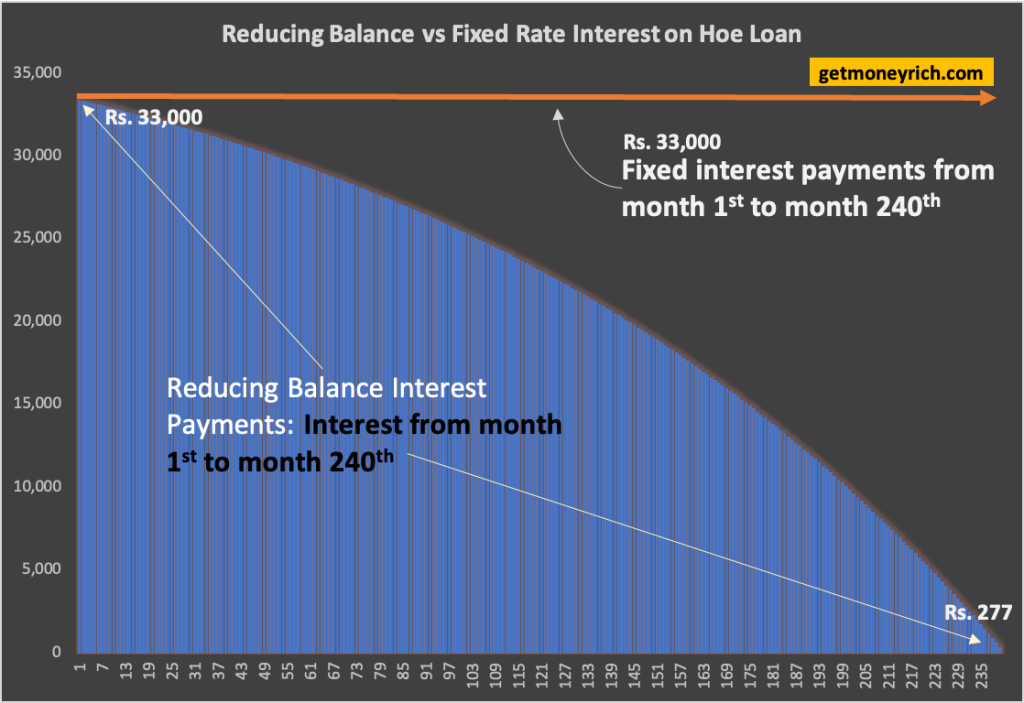

Visualizing the Difference

Fixed vs. Reducing BalanceTo make this clearer, let’s look at a graph I used in an old blog post. It compares the interest payment schedules for a fixed interest loan versus a reducing balance loan.

This graph shows how, in a reducing balance loan (the blue bars and line), the interest you pay each month decreases as the loan balance drops.

In contrast, a fixed interest loan (the orange line) charges the same interest every month, no matter how much you’ve paid off.

For your home loan, you’re on the reducing balance path, which is why the bank said the interest portion will shrink over time.

Will Prepaying Rs. 5,00,000 Save You Interest?

Now, let’s take your question about prepaying Rs. 5,00,000.

The short answer? Yes, it can save you a lot of interest, but let’s see how.

When you prepay Rs. 5,00,000, you reduce the outstanding principal. Since interest is calculated on the remaining balance, a lower principal means less interest each month.

There are two ways banks typically handle prepayments:

- Reduce the EMI, keep the tenure the same: Your monthly EMI drops, but you still pay for 20 years (read about it here).

- Reduce the tenure, keep the EMI the same: You pay the same Rs. 41,822 monthly but clear the loan faster (before 20 years).

Most borrowers prefer the second option because it saves more interest and shortens the loan period.

Let’s estimate the impact using a simplified example.

Suppose you prepay Rs. 5,00,000 after 5 years (in the 61st month). By then, your outstanding principal might be around Rs. 43,76,279.

Prepaying Rs. 5,00,000 reduces the principal to Rs. 38,76,279 (instead of Rs. 43,76,279).

If you keep the EMI at Rs. 41,822, the loan will be paid off faster, by the end of the 17th years.

This will also save you about Rs. 14,70,000 on interest payments.

A rule of thumb, the earlier one makes the payment, more will be the potential savings. In this case, we have assumed a loan prepayment of Rs. 500,000 in the 61st month. Had this prepayment been made in the 37th month (end of the third year), the savings would have been in the tune of Rs. 16,95,000.

Why Reducing Balance Loans Are Borrower-Friendly?

Reducing balance loans, like your home or car loan, are designed to be fairer to borrowers.

Every time you pay an EMI, you take a small bit away from the principal loan balance. This eventually lowers the interest you pay in the next month.

This is why your bank’s Rs. 33,000 interest in the first month will gradually drop, and more of your EMI will go toward paying off the actual loan.

Compare this to a fixed interest loan, where the interest is calculated on the original Rs. 50,00,000 for the entire term.

| Total Interest Paid (Reducing Balance) in 20 Years | Total Interest Paid (Fixed) in 20 Years |

| 50,37,281 | 80,00,000 |

Conclusion

I hope this clears up the confusion about your reducing balance loan and why the interest isn’t just a flat 8% of Rs. 50,00,000.

The reducing balance method saves you money over time by recalculating interest on a smaller principal each month.

And yes, prepaying Rs. 5,00,000 will definitely save you interest, potentially about Rs.14,70,000 if you do it by the end of the fifth year itself.

If you want to play around with the numbers yourself, try the below online EMI calculator.

Reducing Balance Loan Calculator (Online)

Summary:

EMI (₹):

Total Interest (₹):

Total Payment (₹):

Amortization Table:

| Month | Principal (₹) | Interest (₹) | Remaining Balance (₹) |

|---|

Reducing Balance Loan Calculator (Excel)

Easily build a calculator to track your home loan, like a Rs. 50,00,000 loan at 8% over 20 years, with these steps.

- Start Excel: Open a new blank workbook in Excel.

- Input Loan Details: In cells A1 to A3, add labels: “Loan Amount”, “Annual Interest Rate”, “Loan Tenure (Years)”. In B1 to B3, enter values, e.g., 5000000, 0.08, 20.

- Monthly Interest Rate: Label A4 as “Monthly Interest Rate”. In B4, enter

=B2/12(e.g., 8% ÷ 12 = 0.006667). - Total Months: Label A5 as “Total Months”. In B5, enter

=B3*12(e.g., 20 × 12 = 240). - Calculate EMI: Label A6 as “Monthly EMI”. In B6, use

=PMT(B4,B5,-B1)(e.g., ~Rs. 41,822). - Build Amortization Table: In row 8, add headers: A8 (“Month”), B8 (“Opening Balance”), C8 (“EMI”), D8 (“Interest”), E8 (“Principal”), F8 (“Closing Balance”).

- List Months: In A9 to A248, enter 1 to 240 (use

=A8+1in A9, drag down). - Opening Balance: In B9, enter

=B1(Rs. 50,00,000). For B10 down, use=F9. - Enter EMI: In C9 to C248, enter

=B6(e.g., Rs. 41,822). - Calculate Interest: In D9, enter

=B9*B4(e.g., Rs. 33,333). Copy to D248. - Calculate Principal: In E9, enter

=C9-D9(e.g., Rs. 8,489). Copy to E248. - Calculate Closing Balance: In F9, enter

=B9-E9(e.g., Rs. 49,91,511). Copy to F248. - Verify: Ensure F248 (month 240) is near zero, confirming loan repayment.

This calculator shows how interest decreases monthly as the principal reduces.

What’s the the monthly payment for 18mths you can only give me the first and second Month payment.

Principal =153,000

Interest rate=( 7.02% on a reducing balance

4.58% flat rate equivalent)

Period’s of payment = 18months

Calculate on a monthly basis.

Please leave me the answer I will appreciate

How did you get the EMI in reducing method but by hand? not using excel formula please..

Please help explain well to me if I have borrowed 6,000,000/= for 12months how would I calculate the interest on reducing balance if the rate is 10%?

This is so useful to consider taking loans as Sri Lanka is in dire straits and interest rates have gone through the roof! Keep up the good work.

This is how loan are on Whole Life insurance policies

In reducing method how do we get EMI amount and principal amount

Hi,

– EMI calculated is explained in point #2 above.

– Principal amount is the disbursed loan amount.

Thanks for asking

I get 1100000 Rs home loan in 180 month per month 16300 EMI

What interest I paid (loan is Flat Rate)

Loan amount 11000000

EMI per month 16300

Loan paid in 15 years

What interest I paid

Interest = Total Payment – Loan Amount = (16300x12x15 – 11,00,000) = 18,34,000

Thanks for asking.

Mani,

What about if there are a number of payments are missed? Or payments were not made on time? How do we then calculate?

*Because I’m now understanding that, even if no payment is made for months, the interest still has to be calculated and applied to the balance.

Please help me.

Good lecture!

However, I would like to request you to tell how we determine the monthly ‘principal installment’. Like how was rs 8,014 in the example above determined?.

Very useful… Thank you very much. Keep doing what is good for others, helping others and I believe good things will go back to you.

Please get in touch with me so that we can do some business together on some finance calculations.

Sir Can assist me to work out:

Loan : 324,000

Fixed 2.25% for 2 years

How to calculate the loan interest

Thank you for sharing this article! This is what I am looking for. Finally, I found it. Thank you once again.

Sir,

Please give me a calculation on the following data:

Loan amount: Rs.12 crore

Interest: 3.25 on reducing floating interest

Period: 10 years

Loan Payment: Yearly

Thanks,

Dr. Guha

Sir pl guide me as I am going to take car loan of rs630000

Fix %ofintrest 7.35 better or

Somehow similar reducing rate

Sir, i have availed housing loan (staff)for rs. 750000/= with 5% simple rate of interest on reduced balance for 240 months period. Every month 2450/= recovered. 240 months completed but loan was not closed. How sir

I have paid rs. 4250/= erroniouly mentioned as 2450/= sir

Simple Interest = 7,50,000 x 0.05 x 20 = 7,50,000

Total Payment Due = Principal + Interest = 15,00,000

Loan EMI = 15,00,000/(20 x 12) = Rs.6,250

What I’ve answered was based on SIMPLE INTEREST’s concept only.

I’ll need to know more about what was the terms of the “reduced balance”…to attempt that as well.

Sir, thanks for your prompt reply. But the reply was not salved the problem.

750000/= 1st month principle

745500/= 2nd month principle

741000/= 3rd month principle

Like that @ 5% interest apply on only monthly principle amount

THEN HOW MANY YEARS TO CLOSE THE LOAN

Rs 4500/= reduced from principal every month. Kindly help sir,

EMI calculation on “Simple Interest” rates are not done like this. Please see my previous reply.

very nicely explained ,thank you

If someone takes a loan @8% simple interest for Rs 770000 on condition that pricipal amount will be repaid by 92 monthly instalments @Rs 8378 and thereafter the interest to be repaid 60 monthly instalments.How mach interest to be paid?

Simple Interest = 770000 x 8% x (92+60)/12 = Rs.7,80,267

The interest amount of Rs.7,80,267 to be paid back in 60 monthly instalments (@13,004 per month)

really very helpful blog with all maths explained in detail.

good information thanks for posting

Thanks

I Think You Are a Good Teacher

Thanks for liking the work.

it is usefull