Recently we’ve heard the news on RBI‘s announcement of a record dividend payout of INR 2.1 trillion to the Government of India (GOI) for the fiscal year 2023-24. This unprecedented transfer, promises a substantial boost to the government’s fiscal position.

Related to this news, allow me to share with you a few interesting data I was able to collect from the RBI’s annual reports of the past.

Topics:

Point #1: RBI’s Surplus Transfer – Last 20 Year Data

| SL | Year | Total Asset (Cr.) | Total Income (Cr.) | Surplus Payable to GOI (cr.) | Surplus as % of Total Asset | Surplus as % of Total Income |

| 1 | 2023-24 | Data Not Available | Data Not Available | 2,10,000 | Data Not Available | Data Not Available |

| 2 | 2022-23 | 63,44,756 | 2,35,457 | 87,416 | 1.38% | 37.13% |

| 3 | 2021-22 | 61,90,302 | 1,60,112 | 30,307 | 0.49% | 18.93% |

| 4 | 2020-21 | 57,07,669 | 1,33,273 | 99,122 | 1.74% | 74.38% |

| 5 | 2019-20 | 53,34,793 | 1,49,672 | 99,122 | 1.86% | 66.23% |

| 6 | 2018-19 | 41,02,905 | 1,93,036 | 1,47,987 | 3.61% | 76.66% |

| 7 | 2017-18 | 36,17,594 | 78,281 | 40,000 | 1.11% | 51.10% |

| 8 | 2016-17 | 33,04,094 | 61,818 | 30,659 | 0.93% | 49.60% |

| 9 | 2015-16 | 32,43,011 | 80,870 | 65,876 | 2.03% | 81.46% |

| 10 | 2014-15 | 28,89,159 | 79,256 | 65,896 | 2.28% | 83.14% |

| 11 | 2013-14 | 26,24,367 | 64,617 | 52,679 | 2.01% | 81.52% |

| 12 | 2012-13 | 23,90,711 | 45,564 | 33,010 | 1.38% | 72.45% |

| 13 | 2011-12 | 22,08,945 | 26,151 | 16,010 | 0.72% | 61.22% |

| 14 | 2010-11 | 18,04,666 | 23,668 | 15,009 | 0.83% | 63.41% |

| 15 | 2009-10 | 15,53,058 | 27,166 | 18,759 | 1.21% | 69.05% |

| 16 | 2008-09 | 14,08,216 | 33,231 | 25,009 | 1.78% | 75.26% |

| 17 | 2007-08 | 14,62,999 | 21,112 | 15,011 | 1.03% | 71.10% |

| 18 | 2006-07 | 10,01,954 | 52,888 | 45,720 | 4.56% | 86.45% |

| 19 | 2005-06 | 8,08,820 | 14,257 | 8,404 | 1.04% | 58.95% |

| 20 | 2004-05 | 6,82,830 | 12,215 | 5,400 | 0.79% | 44.21% |

Trend in Total Assets and Total Income

- Total Assets: The RBI’s total assets have seen a substantial increase over the years. From ₹6.82 lakh crore in 2004-05, assets have grown to ₹63.44 lakh crore by 2022-23. This growth rate (12.4% CAGR) indicates a significant expansion of the RBI’s balance sheet.

- Total Income: Similarly, the total income of the RBI has also shown an upward trend. In 2004-05, the total income was ₹12,215 crore, which increased to ₹2,35,457 crore in 2022-23. This is an income growth rate of 16.9% CAGR. It is indicative of the RBI’s growing earnings from its various operations, including foreign currency holdings, bond investments, and other activities.

Surplus Payable to the Government

- The surplus payable to the Government of India has fluctuated over the years. Notable peaks include:

- ₹1,47,987 crore in 2018-19.

- ₹99,122 crore in 2020-21 and 2019-20.

- The highest ever, ₹2,10,000 crore, in 2023-24.

- These peaks often correspond to years with significant income and asset growth. It suggest effective asset management and profitable operations by the RBI.

Surplus as a Percentage of Total Assets

- This metric indicates how much of the RBI’s assets were turned into surplus. Generally, this percentage has remained relatively low, often below 2%. Notable exceptions include:

- 2018-19, with 3.61%

- 2006-07, with 4.56%

- Average Between 2004 to 2024: 1.62%

- The low percentages in most years highlight that while the RBI’s operations generate significant surplus, they form a small fraction of the overall asset base.

Surplus as a Percentage of Total Income

- The surplus as a percentage of total income provides insight into the efficiency of the RBI’s income generation in relation to its surplus. This percentage has varied widely, with notable highs:

- 86.45% in 2006-07.

- 83.14% in 2014-15.

- 81.46% in 2015-16.

- High percentages in these years suggest that a substantial portion of the RBI’s income was effectively converted into surplus, reflecting efficient financial management.

Key Observations

- Record Dividend in 2023-24: The ₹2.1 trillion dividend in 2023-24 is unprecedented, in absolute terms. But to judge if RBI can really afford to pay this dividend, we’ll have to wait for the release of “Income” and “Total Asset” data by the RBI. If the “Surplus as % of Asset” and “Surplus as % of Income” is higher than the last 20-year trend, only then we can actually tag it as unprecedented and doubt its issuance.

- Income vs. Surplus Fluctuations: While the RBI’s income has generally increased, the surplus payable to the government has seen more volatility. This suggests that specific years had exceptional factors (like high earnings from certain operations) leading to higher surpluses.

- Efficiency Indicators: The years with high surplus percentages relative to income (like 2006-07, 2014-15) indicate periods of highly efficient financial performance where a large part of income translated into surplus.

The data reflects the RBI’s growing financial capacity and its ability to generate significant surpluses from its operations. The record ₹2.1 trillion surplus in 2023-24 underscores an exceptionally profitable year, contributing substantially to the government’s fiscal resources and helping manage the fiscal deficit. This financial performance is crucial for maintaining economic stability and supporting government expenditures.

Point #2: Details of RBI’s Sources of Income

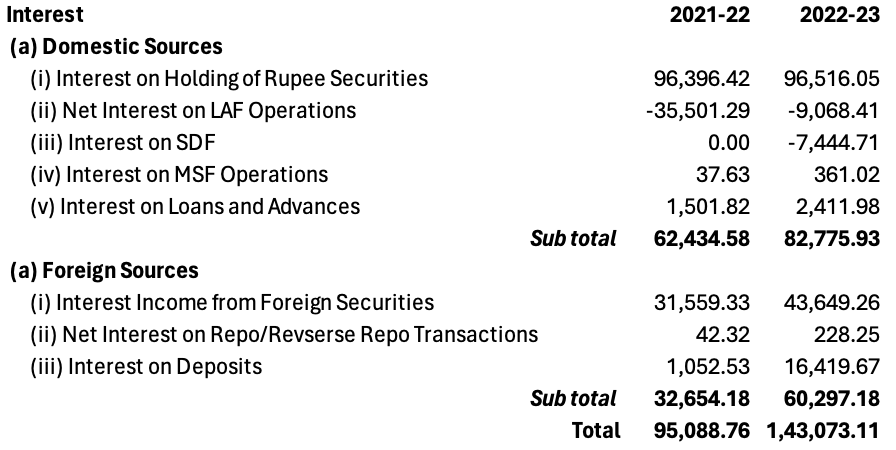

2.1 Interest Income Overview (Domestic Sources)

- Interest on Holding of Rupee Securities: FY 2022-23: ₹96,516.05 crore and FY 2021-22: ₹96,396.42 crore. This consistent figure represents the interest earned from various government securities held by the RBI. It shows showing a stable income stream from domestic bonds and treasury holdings.

- Net Interest on LAF Operations: FY 2022-23: -₹9,068.41 crore and FY 2021-22: -₹35,501.29 crore. The Liquidity Adjustment Facility (LAF) includes operations like repo and reverse repo. The negative values indicate that the RBI paid more interest on absorbing liquidity than it earned from injecting liquidity. Though the cost decreased significantly in FY 2022-23.

- It means that the RBI had to pay more money to banks to keep their extra funds (liquidity) safe than it made from lending money to banks. Essentially, the RBI was spending more to manage excess cash in the system than it was earning from providing loans to banks. This scenario often occurs during times when there is an excess of money in the banking system, and the RBI needs to soak up this surplus to maintain economic stability.

- Interest on SDF: FY 2022-23: -₹7,444.71 crore and FY 2021-22: ₹0.00 crore. The Standing Deposit Facility (SDF) involves absorbing surplus liquidity from banks without offering collateral. The introduction of a cost in FY 2022-23 indicates an added expense for managing excess liquidity.

- The Standing Deposit Facility (SDF) is a tool used by the RBI to manage extra cash in the banking system. When banks have more money than they need, the RBI can absorb this surplus cash without giving anything in return, like securities or other assets. This helps the RBI control the amount of money in circulation and maintain economic stability, without the need to provide collateral.

- Interest on MSF Operations: FY 2022-23: ₹361.02 crore and FY 2021-22: ₹37.63 crore. The Marginal Standing Facility (MSF) allows banks to borrow overnight funds from the RBI against government securities. The increase reflects higher income from these short-term borrowings.

- Interest on Loans and Advances: FY 2022-23: ₹2,411.98 crore and FY 2021-22: ₹1,501.82 crore. This includes interest from various loans and advances provided to state governments and other institutions. The increase indicates higher lending activity or rates.

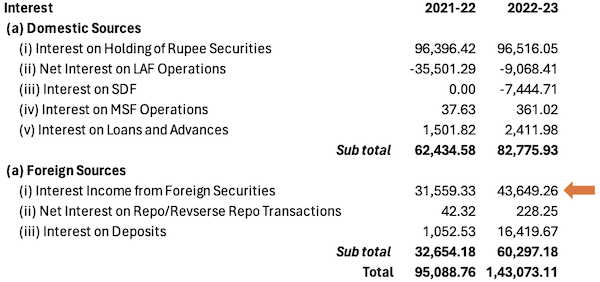

2.2 Interest Income Overview (Foreign Sources)

- Interest Income from Foreign Securities: FY 2022-23: ₹43,649.26 crore and FY 2021-22: ₹31,559.33 crore. Earnings from the RBI’s investment in foreign bonds and securities increased significantly. It reflects higher interest rates globally, particularly in the US and other major economies. RBI made a lot more money from its investments in foreign bonds and securities. This happened because interest rates in big economies like the US went up. When interest rates are higher, the RBI earns more money from the bonds and securities it holds in those countries.

- Net Interest on Repo/Reverse Repo Transactions: FY 2022-23: ₹228.25 crore and FY 2021-22: ₹42.32 crore. Income from repurchase agreements involving foreign securities. The increase indicates more active participation in international repo markets. It means, RBI made more money from short-term loans where it temporarily sells its foreign securities and agrees to buy them back later. The increase in income shows that the RBI has been more actively involved in these types of transactions in international markets. It is there where they borrow money using their foreign assets as security.

- Interest on Deposits: FY 2022-23: ₹16,419.67 crore and FY 2021-22: ₹1,052.53 crore. Earnings from deposits held in foreign banks rose significantly. It points to higher deposit rates or increased foreign deposit holdings. It means, RBI made a lot more money from keeping its funds in foreign banks. This could be because the interest rates for deposits in these banks went up. It can also be due the RBI putting more money into these foreign bank accounts, earning more interest as a result.

2.3 Other Income Overview (Domestic Sources)

- Exchange (0.00 for both years): It refers to the revenue generated by the RBI through differences in currency exchange rates. In the fiscal years 2021-22 and 2022-23, there was no income generated from exchange differences. It indicates that the RBI did not earn any profits or incur any losses from fluctuations in currency exchange rates during those periods.

- Discount (403.76 crore in 2021-22, 0 in 2022-23): In 2021-22, RBI earned 403.76 crore from discounts. This income was absent in 2022-23. Discounts can occur when the RBI buys government bonds at a lower price than their face value. This way it earns income from the difference upon maturity. For example, if the RBI purchases a bond worth 100 rupees for 95 rupees, it earns a 5 rupee discount. This income contributes to the RBI’s overall revenue.

- Commission (3058.09 crore in 2021-22, 3469.14 crore in 2022-23): Commission income for the RBI can arise from managing government transactions or providing banking services. For instance, if the RBI facilitates a government bond sale, it may earn a commission fee based on the transaction’s value. Similarly, offering banking services like processing payments or managing accounts can generate commission revenue.

- Rent Realised (11.38 crore in 2021-22, 8.99 crore in 2022-23): Rent realized by the RBI involves earning income from properties it owns or leases out. For instance, if the RBI rents out office space or residential properties it owns, the rental payments it receives constitute rent realized.

- Profit/Loss on Sale and Redemption of Rupee Securities (6028.19 crore in 2021-22, -222.86 crore in 2022-23): The RBI can earn profit from selling rupee securities at a higher price than their purchase cost. For example, if it sells government bonds at a price higher than their acquisition cost, the difference constitutes a profit. Conversely, if it sells securities at a lower price, it incurs a loss.

- Depreciation on Rupee Securities Inter Portfolio Transfer (-20.07 crore in 2021-22, -110.67 crore in 2022-23): It represents a decrease in the value of securities transferred between RBI portfolios. For instance, if the RBI transfers government bonds from one portfolio to another and their value decreases during the transfer, the difference constitutes depreciation. This expense reduces the RBI’s overall income.

- Amortisation of Premium/Discount on Rupee Securities (-1717.97 crore in 2021-22, -2264.19 crore in 2022-23): It involves gradually writing off the difference between the purchase price and face value of securities over their maturity period. For instance, if the RBI buys government bonds at a premium (higher than face value), it spreads the premium amount over the bond’s lifespan. This process reduces the premium’s impact on income upfront, distributing it evenly over time.

- Profit/Loss on Sale of Bank’s Property (6.72 crore in 2021-22, 2.45 crore in 2022-23): It refers to the income earned or lost when the RBI sells its owned properties. For example, if the RBI sells a piece of land or a building at a higher price than its acquisition cost, the difference constitutes a profit. Conversely, if it sells the property at a lower price, it incurs a loss.

- Provision No Longer Required and Miscellaneous Income (325.09 crore in 2021-22, -330.07 crore in 2022-23): It includes funds previously set aside but no longer needed and other miscellaneous earnings. For example, if the RBI had reserved funds for potential losses that didn’t materialize, releasing these provisions would add to its income. Additionally, miscellaneous income might include various smaller sources such as fines or penalties.

2.3 Other Income Overview (Foreign Sources)

- Exchange gain/loss from Foreign Exchange transactions (68,990 crore in 2021-22, 1,03,208 crore in 2022-23): It occurs when the RBI buys or sells foreign currencies. For example, if the RBI buys dollars when the exchange rate is low and sells them when the rate is higher, it makes a profit (exchange gain). Conversely, if the exchange rate drops, it incurs a loss. These transactions significantly impact the RBI’s overall income.

Point #3: Explanation of INR 2.1 Trillion Dividend

Before the explanation, I’ll first do a back calculation. I’ll try to estimate what could have been the income level of RBI in the FY 2023-24. I’m assuming that the RBI has paid the hefty dividend out of the income it has earned in the FY 2023-24. Ms. Latha Venkatesh of CNBCTV18 has reasoned the dividend payout in these lines in her article.

| Year | Surplus Payable to GOI ( Cr.) | Surplus as % of Total Income | Remarks |

| 2003-04 | 5,400 | 37.70% | Lok Sabha Elections Held in Next FY |

| 2004-05 | 5,400 | 44.21% | – |

| 2005-06 | 8,404 | 58.95% | – |

| 2006-07 | 45,720 | 86.45% | – |

| 2007-08 | 15,011 | 71.10% | – |

| 2008-09 | 25,009 | 75.26% | Lok Sabha Elections Held in Next FY |

| 2009-10 | 18,759 | 69.05% | – |

| 2010-11 | 15,009 | 63.41% | – |

| 2011-12 | 16,010 | 61.22% | – |

| 2012-13 | 33,010 | 72.45% | – |

| 2013-14 | 52,679 | 81.52% | Lok Sabha Elections Held in Next FY |

| 2014-15 | 65,896 | 83.14% | – |

| 2015-16 | 65,876 | 81.46% | – |

| 2016-17 | 30,659 | 49.60% | – |

| 2017-18 | 40,000 | 51.10% | – |

| 2018-19 | 1,47,987 | 76.66% | Lok Sabha Elections Held in Next FY |

| 2019-20 | 99,122 | 66.23% | – |

| 2020-21 | 99,122 | 74.38% | – |

| 2021-22 | 30,307 | 18.93% | – |

| 2022-23 | 87,416 | 37.13% | – |

| 2023-24 | 2,10,000 | 82% (Assumed) | Lok Sabha Elections Held in Next FY |

The above table highlights the FY’s after which there were General Elections held in India. In each of these years, the surplus paid as the percentage of income was higher than other years (2003-04 was an exception).

Taking these percentage values as a benchmark, I’m assuming that in FY24, the RBI board has decided to pay 85% of their income as dividend to the Government.

If RBI has decided to pay INR 2.1 Trillion as dividend and 85% is the payout percentage, then the estimated total income of the RBI would be around INR 2.47 Trillion.

In Ms.Latha Venkatesh’s article, she has discussed a rise in the following sources of income for the RBI in FY24:

- Interest Income from Foreign Securities: Ms.Latha writes that in FY23, “the average US Fed funds rate in FY23 was around 2.5%, while in FY24 the average was 5%.” This is an indication that RBI’s Interest income from foreign securities must have increased considerably. In the FY23, this component was about Rs.43,649.26 Crores. Considering the rise in bond yields, In FY24, this component can rise to about Rs.80,000 crores.

- Exchange gain from Foreign Exchange transactions (Sale of dollars): In the FY24, Ms.Latha write about RBI selling about $153 Billion worth of USD. These dollar transactions have been done at a profit as compared to its average purchased price. Average buy price of the dollar was at about $74 while selling happened at about $82. Considering this data, in FY24, the exchange gain for RBI would be close to Rs.1.15 Lakh Crore. Ms.Latha’s estimate is about Rs.1.2 Lakh crore assuming a 16% jump in income from FY23 numbers.

In total, the above two income sources alone is likely to generate Rs.2.0 Lakh Crore (Rs.0.8 + Rs.1.2). Hence, I think RBI’s Rs.2.1 lakh Crore is high but not unreasonable. Nevertheless, as RBI releases is Annual report for the FY23-24, more clarity will emerge. It is also true RBI is unlikely to make such high dividend payouts to the GOI in the coming financial years. Hence, the fiscal deficit will come down only for this year (due to this dividend payout). For the other coming years, RBI dividend pay is unlikely to be so high.

Have a happy investing.

Suggested Reading: