What makes an economy?

You can think about an economy as a giant engine powered by human interaction.

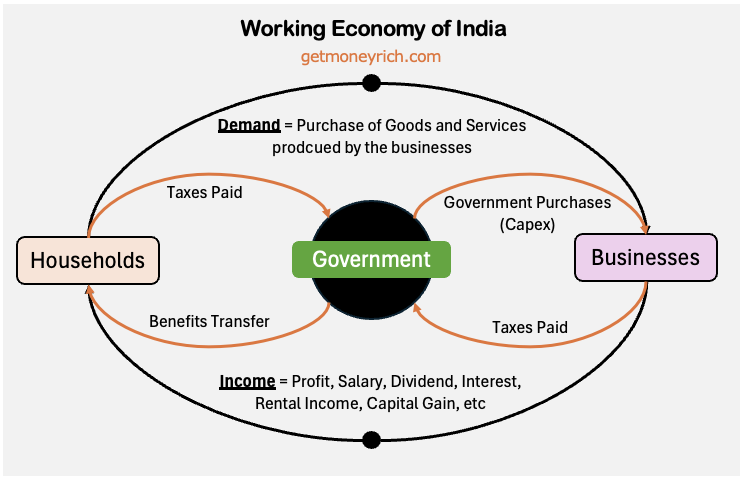

It is simply the sum of all transactions that happen between these three entities:

- households,

- Businesses, and

- The government.

Whenever you buy a coffee, do a job, or sell a soap, you are “making” the economy happen.

Economy is not just about the money in the bank; it represents the collective resources, goods, and services that a society produces (supply) and consumes (demand) to survive and thrive.

This system functions on supply and demand.

- Businesses create things (supply) that people need or want (demand).

- You trade your time and skills for money.

- Now, when you’ve earned money, you trade that money for the things you need.

Money is that essential tool (like the oil in the engine) that makes the exchange of things easier and convenient. It is easier than bartering chickens for air travel (for example).

If people spend money, businesses grow and hire more people. If spending stops, the engine slows down. This is the reason why the government gives so much emphasis to “consumption.”

Ultimately, the most important rule is that one person’s spending is another person’s income.

It is a continuous loop relying on trust and circulation.

When resources are turned into valuable products efficiently, the standard of living generally rises.

The economy is the direct result of millions of individual choices, including yours, interacting every single day.

Let’s bring GDP and Inflation into this picture:

- GDP: Every time you (a household) buy a phone from a Business, or the Government pays a construction firm to build a road, that value is added to the GDP. A growing GDP indicates that the economy is active and expanding.

- Inflation: If Households and the Government suddenly want to buy more stuff than Businesses can produce, there is a shortage of supply. Businesses then raise their prices because their products are in high demand. This general rise in prices is a form of inflation.