Introduction

India’s economy (GDP) is growing at 8.2% in the July–September quarter (read here), which sounds like good news.

On paper, it reinforced the narrative of India as the fastest-growing major economy. It suggests businesses are producing more, people are spending, and the economy is moving faster than expected.

For many of us, a GDP of 8%+ alone feels reassuring, right? It is proof that India is doing well despite global uncertainty.

But economic numbers often need context. I think it must always be read with a pinch of salt. Several economists have pointed towards the use of a low GDP deflator to amplify the real growth rate.

What is the GDP deflator?

It is basically inflation, but not consumer inflation. Let’s understand it using an example.

Suppose our economy produced a set of goods worth Rs. 100 last year and Rs. 110 this year. In this example, the nominal growth is 10%. Now, suppose the prices of this set of goods rose 4% during this year (inflation). In this case, the GDP deflator would be 4%. To find the real growth rate, we must remove the price-rise effect from the GDP.

Real Growth = Nominal Growth (10%) – GDP Deflator (4%) = 6%

If a government decides to use a lower GDP Deflator (for some reason), it will make the real growth look stronger.

According to sources, the GDP Deflator used by the Indian government for the July-September quarter was 0.5% (read here).

In India, when average inflation stays in a range of 4-6%, a 0.5% GDP deflator sounds questionable.

This 8.2% GDP growth figure looks strong, partly because the GDP deflator was low. It also means that the prices did not rise much during the period. When inflation is low, real growth automatically looks higher (see the formula).

The economy did grow, but not all of that strength came from a big jump in actual activity, like higher factory outputs or companies investing more.

There indeed is a gap between what people experience on the ground and what the GDP numbers report. Indicators that track day-to-day economic health factors like factory output, exports, and business confidence have slowed.

From a long-term investor’s point of view, strong GDP growth, a weakening rupee, and an RBI rate cut are not separate signals; they are connected pieces of the same story. They are telling us about where the economy is headed and how risks and opportunities are shaping up.

Rupee Falling Below 90

When the rupee slipped past 90 against the dollar, it raised concerns because round numbers matter psychologically. Here is a table that shows how INR devalued with respect to USD since 1975.

| SL | Year | INR/USD Rate | Remarks |

| 1 | 2026 | 90 | First Touched 90s |

| 2 | 2022 | 80 | First Touched 80s |

| 3 | 2018 | 70 | First Touched 70s |

| 4 | 2013 | 60 | First Touched 60s |

| 5 | 2011 | 50 | First Touched 50s |

| 6 | 1999 | 40 | First Touched 40s |

| 7 | 1993 | 30 | First Touched 30s |

| 8 | 1992 | 20 | First Touched 30s |

| 9 | 1984 | 10 | First Touched 10s |

| 10 | 1975 | 7.9 | Stayed below double-digit |

Weakening of the rupee has always been a topic of politically charged debate.

- While some see the move (Rupee fall) as evidence of pressure from global factors. There can be factors like a strong dollar, capital outflows, and trade tariffs. Some people will also interpret it as a calibrated tolerance by the RBI.

- For some, a weaker rupee means imports become more expensive. Imports like fuel, electronics, and raw materials will cost more in India. Over time, this price rise will also affect the profits and margins of companies.

In today’s terms, how many nutral experts see INR becoming 90 to a dollar?

First of all, it does not mean the RBI has lost control. RBI is not sitting idle.

- RBI has kept a large foreign exchange reserves, which act like a financial safety buffer.

- The central bank is also actively managing liquidity and stepping into markets when needed.

The rupee’s fall looks more like something the RBI is allowing rather than something it cannot stop.

Why would a central bank allow this? Because fighting every currency move can drain reserves and hurt growth. Instead, a slightly weaker rupee can help exporters sell goods abroad more competitively.

But this strategy works only if managed carefully (it is like a double-edged sword).

If the currency keeps weakening without clear signals, investors can lose confidence, and eventually, the whole financial market could collapse. That will be a mayhem scenario.

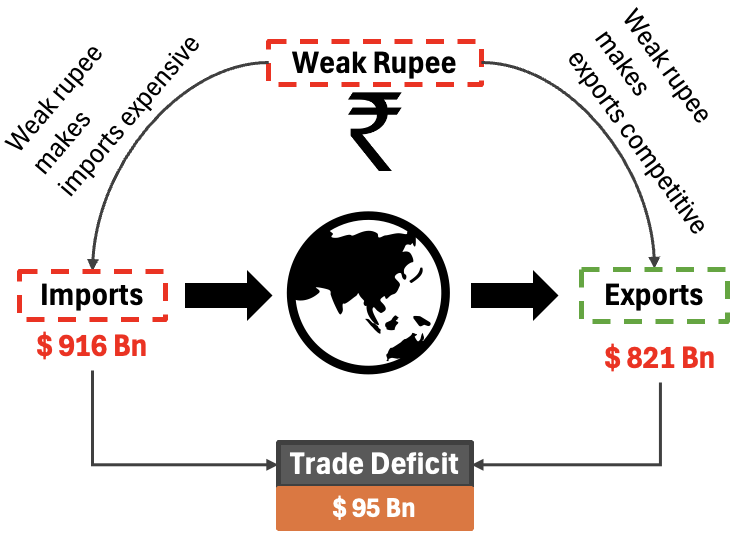

Note: On one side, a weak Indian rupee is good for exports, but on the other side is makes imports expensive. In a country like India, whose trade deficit (export minus import) is negative, a weak Rupee is not good. While it makes our software and textiles cheaper for foreign buyers, that gain is wiped out by our massive imports like crude oil, electronics, gold, and even the purchase of US-linked assets. We must pay for these in Dollars. When the Rupee is falling, prices of all these things soar. It hits everything in India, from transport to groceries (inflation). Until India fixes the trade deficit, currency depreciation will remain a tax on the public rather than a competitive win.

Understanding the RBI’s Rate Cut

Let’s talk about the RBI’s decision to cut interest rates by 0.25%.

Interest rates are essentially the “price of money.” When they come down, borrowing becomes cheaper.

- For a business, this means loans for setting up factories or expanding operations cost less.

- For households, it means lower EMIs on home, car, or personal loans, leaving more money available to spend elsewhere.

The RBI took this step because inflation has cooled significantly. When price rise feels is in control, RBI gets room to focus on growth rather than worrying about high inflation. Lowering of rates is like the RBI is saying: prices are under control for now, so we can afford to give the economy some support.

However, we must also know that this rate cut is not because the economy is doing exceptionally well. The rate was brought because the RBI wants to prevent growth from slowing down in the months ahead.

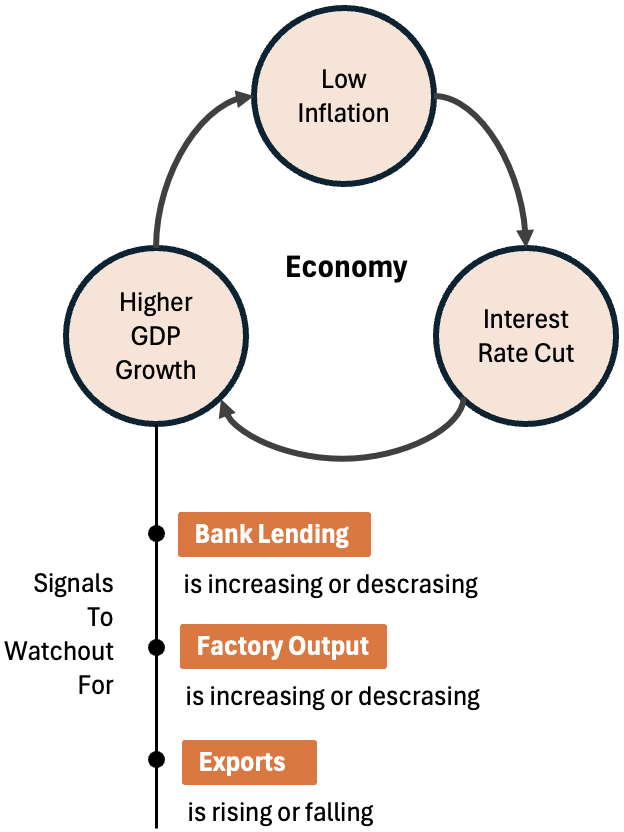

Despite high GDP numbers, several warning signals are flashing beneath the surface.

- Bank lending has not increased meaningfully. It tells us that the businesses are still cautious about taking fresh loans.

- Factory output is also weaker than before. It is also suggesting that the demand is not as strong as the GDP growth numbers are trying to say.

- Exports are another area of concern. Shipments to the U.S. have fallen sharply, partly due to higher tariffs. When exports slow, it directly affects manufacturing jobs, corporate earnings, and investment plans.

These are not just any abstract indicators; they directly influence jobs, salaries, and the future spending power of people, businesses, and the government across the economy.

The rate cut is the RBI’s attempt to stay ahead of the curve.

By lowering rates now, it hopes to encourage borrowing and investment before a slowdown becomes more visible.

What This Means for the Indian Economy

So, what can we conclude from all this data?

India’s economy is not in trouble, but it is also not as strong as the GDP growth number might suggest.

A large part of the current momentum is coming from government spending and short-term boosts to demand. At the same time, areas (see the following 3 points) that usually support long-term strength are still looking weak.

- Private investment,

- Exports, and

- Sustained credit growth

Government-led growth can provide support, but it cannot carry the economy forever. For growth to remain healthy over time, businesses must feel confident enough to invest, hire, and expand on their own.

When the businesses are not spending freely, it tells us that uncertainty still exists beneath the surface.

Can This Growth Last?

The key issue now is sustainability.

Some of the recent strength has come from festive-season spending and favorable comparisons with last year’s numbers. These effects do not last.

Once they fade, the economy will need genuine demand and investment to keep growth steady.

- Lower interest rates are meant to help here.

- Cheaper loans only work if businesses see enough demand to justify expansion and if banks are willing to lend.

- Similarly, consumers spend more when they feel secure about jobs and income.

Whether these conditions fall into place will determine how the economy performs in the next few quarters.

RBI is also Careful

RBI is playing the growth vs inflation game carefully.

- On one side, they want to support growth by cutting rates and allowing some flexibility in the currency.

- On the other hand, they must ensure inflation stays under control and financial stability is not compromised.

Getting this balance right is difficult, especially when leaders like Trump, Putin, and Xi are shaping the narratives.

I think internally, RBI must be feeling cautious rather than confident.

By acting early, it is trying to prevent small cracks from widening. This approach reduces the risk of sharper interventions later, but it also signals that policymakers are aware of underlying vulnerabilities.

Have a happy investing.

![Income Tax Slabs: Tax Liability Comparison Between 2020 and 2019 [Calculator]](https://getmoneyrich.com/wp-content/uploads/2020/02/Income-tax-slabs-Image-300x195.png)