Introduction

The fear is real.

Over the last year or so, every time I read a post on the IT sector, it talks almost about the same thing.

Every second LinkedIn post, every business news headline, and every analyst report seems to be signalling the same thing. Artificial Intelligence (AI) is going to fundamentally destroy the Indian IT services industry as we know it.

Some people are saying TCS, Infosys, Wipro, and their peers are heading for a slow, painful decline.

That is a strong claim, and for investors like me, it calls for action.

But since my 15+ years of investing experience, I’ve also seen that investing in such times, in top companies of a distressed sector, gives the best returns in the long term.

I have been following the Indian IT sector for a while now. I think the fear is being exaggerated, not because AI is not disruptive, but because people are forgetting history.

This industry has already been through multiple waves of technology disruption.

- Each time, the narrative was similar.

- Each time, the industry found a way to absorb the shock and rebuild itself around the new reality.

What I want to do in this post is share with you the history. I’ll then compare it with what is happening today with AI.

So let’s start.

The Foundation Was Built on on-premises everything

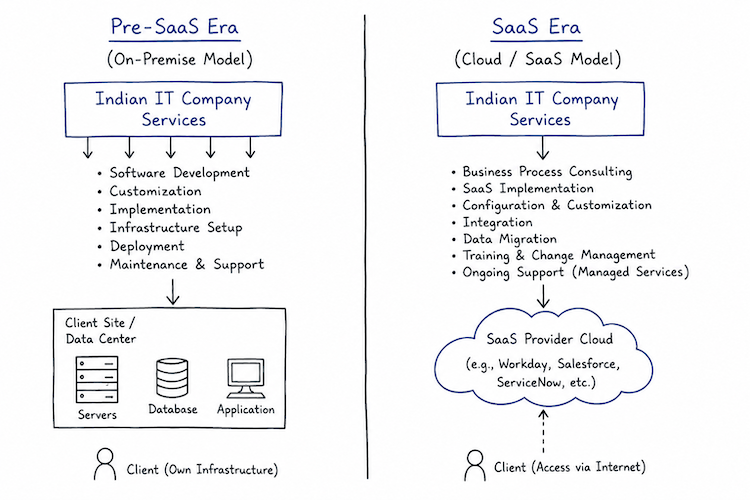

To understand why AI feels so threatening today, you first need to understand what Indian IT companies were actually selling for the first two decades of their existence.

In the 1990s and early 2000s,

Enterprise technology looked very different from what we see today.

Large corporations in the United States, the United Kingdom, and across Europe ran most of their critical business systems on their own infrastructure.

Every major bank, insurance company, telecom operator, and manufacturing firm maintained physical servers on their premises, managed their own databases, and ran their own ERP systems.

They used to keep an entire IT department just to keep their IT infrastructure working.

This created a situation where enterprise software had to be purchased as a product, installed physically, customised to fit the company’s specific workflows, and then maintained indefinitely.

SAP, Oracle, PeopleSoft, Siebel, these were the platforms that ran global enterprises.

Deploying them was complicated, time-consuming, and expensive.

American and European companies quickly realised that sending this work offshore to India was far more cost-effective than hiring domestically.

That is exactly where companies like TCS, Infosys, Wipro, and Tech Mahindra stepped in.

They built their entire business model on being the trusted, affordable, technically capable partner for exactly this kind of work. They offered their customers the following as their business offering:

- Implementation,

- Customisation,

- Application maintenance,

- Infrastructure management,

- Testing,

- Production support, and

- Offshore development.

The economics for our IT companies were simple.

These companies are billed by the hour and by headcount.

The larger the team, the larger the contract.

- Infosys alone went from roughly 1,000 employees in 1993 to over 75,000 by 2007.

- TCS crossed 100,000 employees around the same time.

The Indian IT industry grew into a $50 billion plus sector based on this model.

The model worked because enterprises genuinely needed large, sustained human effort to keep their complex on-premise technology ecosystems running.

Example: Infosys is working for General Electric.

In the pre-SaaS era, Infosys teams helped install, customize, maintain, and support software running inside GE’s own data centers and office infrastructure through long-term manpower-based IT service contracts. The type of system helped General Electric manage its business operations like finance, employee records, inventory, manufacturing, internal workflows, and enterprise data across different offices and factories. These are what we used to call ERP (Enterprise Resource Planning) systems offered by companies like SAP, Oracle, PeopleSoft, Baan, etc.

Then SaaS Arrived

People said the same things they are saying now about AI.

Around 2007 to 2010, something started shifting quietly in the enterprise technology world.

Salesforce had already been building its cloud-based CRM platform since 1999. But it was only in the late 2000s that cloud and SaaS genuinely started threatening the on-premise model.

Amazon Web Services launched in 2006 and began showing enterprises that they did not need to own physical servers anymore.

Workday was founded in 2005 specifically to replace on-premise HR and finance systems with a cloud-delivered alternative.

ServiceNow, SuccessFactors, and later Microsoft’s Azure and Office 365 all followed the same logic.

The fear at the time was very similar to what we are hearing about AI today. If enterprises no longer needed to install and maintain software on their own infrastructure, what would happen to all those implementation and maintenance contracts?

- If Workday replaced PeopleSoft, you would not need armies of PeopleSoft consultants anymore.

- If Salesforce replaced on-premise CRM, those customisation and support projects would shrink.

The argument was that SaaS would standardise and commoditise enterprise software, dramatically reducing the services opportunity.

And to be fair, this fear was not irrational.

The business model really was under pressure. Some of the largest contracts in Indian IT history were long-term application maintenance and infrastructure management deals. This was precisely the kind of work that cloud and SaaS were making less necessary.

Example: Deloitte is implementing Workday for Walmart.

In the SaaS era, Deloitte helped Walmart migrate HR systems to the Workday cloud. They used to configure workflows, integrate enterprise systems, train employees, and provide ongoing support instead of managing Walmart’s own servers. The system helped Walmart manage employee-related operations like hiring, payroll, attendance, performance tracking, scheduling, and HR workflows through a cloud-based platform.

What Actually Happened Is the More Important Story

When people spread a narrative that the Indian IT Sector may die a slow death, I think they consistently miss a point.

Technology transitions does not eliminate the need for services.

Yes, they can transform what those services look like, but the need for IT services will be there.

When a mid-sized American insurance company decided to move from an on-premise HR platform to Workday, it did not just flip a switch.

- It had fifteen years of employee data sitting in a legacy system.

- It had custom payroll rules built around local tax regulations across twelve states.

- It had integrations connecting HR data to finance systems, compliance systems, and third-party benefits providers.

- Its HR team had workflows built around the old system that now needed to be redesigned entirely.

None of that complexity disappeared just because SAP (ERP) became obsolete and Workday (SaaS) was the new tech.

When ERP died, and SaaS came, our consulting and IT services firms built entire practices around SaaS implementation.

Deloitte, Accenture, Infosys, Wipro, and Capgemini all of them developed dedicated Workday, Salesforce, and ServiceNow practices.

- Infosys built a major Salesforce practice and became one of the largest Salesforce implementation partners in the world.

- TCS built cloud migration competency.

- Wipro invested in AWS and Azure partnerships aggressively.

The revenue mix changed. The skills required changed. The project profiles changed. But the overall demand for skilled technology services did not collapse. It has only evolved more.

By 2020, the Indian IT industry had grown to over $190 billion in annual revenue.

It was significantly larger than it was before the SaaS disruption began.

That is the number people forget when they predict collapse.

Why AI Feels Different — And Why That Feeling Is Partly Justified

AI is not SaaS. I’ll not deny that.

So let’s start with this premise.

AI is genuinely different from earlier technology transitions in one important way.

Previous disruptions (Y2K, the internet, SaaS, cloud) changed where software ran and how it was delivered.

They did not change the fundamental nature of the human work required to build, implement, and maintain that software.

AI changes that.

How the work is done today (Pre-AI Era):

- A developer today uses GitHub Copilot to write code,

- A testing team uses AI tools to auto-generate test cases,

- A support team uses AI agents to resolve first and second-level tickets automatically.

The actual knowledge work that Indian IT companies billed for is being compressed.

Not eliminated, but compressed.

A team that previously needed 80 engineers to deliver a project might now be able to deliver the same output with 45 engineers using AI tools.

That has direct implications for revenue per employee, for headcount growth, and for the traditional outsourcing economics that made Indian IT companies so profitable.

Nasscom and various industry analysts have flagged this concern explicitly.

Infosys CEO Salil Parekh acknowledged in recent earnings calls that AI productivity tools are changing how work gets done internally.

TCS has spoken about reskilling programmes at scale.

These are not small operational adjustments. They are signs that the industry knows its cost and delivery model is under genuine pressure.

So yes, the AI disruption is deeper in a specific way. It touches the unit economics of the business more directly than SaaS did.

Story From The Demand Side of AI

Here is where I think the collapse narrative goes wrong.

AI is not just disrupting IT services; it is also creating enormous new demand for technology work.

And much of that demand will flow through the same Indian IT companies that people are predicting will decline.

Think about what large enterprises (Client side) actually need to do right now. Most of them are nowhere near being AI-ready.

- Their data is sitting in fragmented legacy systems.

- Their infrastructure was not designed for AI workloads.

- Their governance frameworks have no concept of AI risk or model accountability.

- Their workforce has no training in AI-assisted workflows.

- Their security posture has not been updated to handle the risks that AI systems introduce.

Fixing all of this requires enormous amounts of skilled technology work.

They will need the following:

- Data modernisation,

- Cloud infrastructure upgrades,

- AI model integration,

- Custom AI agent development,

- Enterprise AI governance frameworks,

- Training, and

- long-term AI operations support.

These are not simple consulting engagements.

These are big transformation programmes worth hundreds of millions of dollars for large enterprises.

And which companies have the global delivery scale, deep enterprise relationships, compliance expertise, and the ability to manage complex technology transitions at scale?

You guessed it, the same Indian IT companies people are writing off.

Gartner estimated that global AI spending across enterprises will reach well over $500 billion by 2027. A significant share of that will flow into implementation, integration, and transformation services.

That is the new SaaS services economy.

The only difference is, this time it is built around AI platforms (like OpenAI, Anthropic Claude, Google Gemini, etc) instead of cloud SaaS platforms (Salesforce, Workday, ServiceNow, etc).

| AI platforms | Cloud SaaS platforms |

| Examples: OpenAI, Anthropic (Claude), Google Gemini, Microsoft Azure AI, AWS Bedrock, Meta Llama, Mistral AI, Cohere, Databricks, Hugging Face, etc | Examples: Salesforce, Workday, ServiceNow, SAP S/4HANA Cloud, Microsoft 365, Oracle Cloud, SuccessFactors, Zendesk, etc |

The Pattern Is Consistent — But Execution Speed Matters More This Time

When I look at the current AI transition and compare it with the SaaS transition, the underlying pattern is almost identical.

In the SaaS era, platforms like Salesforce, Workday, and ServiceNow themselves used to capture the product value.

But the services layer around those platforms, like implementation, integration, migration, customisation, and managed services, used to go to IT services companies.

Indian IT firms eventually figured out that strategy and built very large practices around it.

In the AI era, platforms like OpenAI, Anthropic, Google Gemini, Microsoft Azure AI, AWS Bedrock are capturing the foundational model value.

But enterprise AI adoption requires a services layer on top of those platforms. That is the opportunity for IT services companies.

But there is a difference between SaaS and AI Transition:

| SaaS Transition | AI Transition |

| SaaS transition played out over roughly a decade, giving Indian IT companies time to adjust gradually | The AI transition is moving faster. Product capabilities are advancing more quickly than enterprise adoption can keep up with. |

What does it mean?

Companies that move slowly will be left behind more quickly than they were in the SaaS era.

This is the reason why I think in this AI era, new leaders will emerge. It is not that TCS, Infosys, and Wipro would go away; if they adopt the AI wave faster, they will continue to dominate the sector for another 10 years at least (till a new disruption comes).

But I’m not sure if such big companies are agile enough to mould themselves into this new AI avatar. I hope they do, but I’m not sure. This is the reason why I’ve shifted all my IT Sector holdings to IT Exchange Traded Funds.

What Could Actually Go Wrong

Let’s also play the devil’s advocate.

The scenario that should genuinely concern Indian IT companies is not that AI destroys all service work overnight. That is not how enterprise technology transitions work.

The real risk is a slower, more structural margin compression over five to seven years as AI tools reduce the billing hours required for standard IT work.

Today, our IT companies bill their client for the following services:

- Code development,

- Testing,

- Documentation,

- Tier-1 support.

If TCS, Infosys, and Wipro continue to grow headcount at historical rates while AI compresses productivity economics, the revenue per employee mathematics starts working against them.

Their cost model, which is fundamentally built on people, becomes harder to sustain if clients are paying for fewer hours to get the same output.

The companies that will come out of this transition well are the ones that genuinely change their delivery model.

These companies will move from headcount-driven execution toward outcome-driven and IP-driven delivery. They will be building proprietary AI tools. They would create specialised AI practices with talents that are genuinely skilled.

This is what used to happen in the early era of IT revolutions. Only the best brains are used to get code developer roles. A similar kind of developer role (thinking power) is required again to build new and innovative AI tools.

I think again, the IISc and IIT level engineers will be required to build AI-based tools.

TCS, Infosys, and Wipro all have the resources, the client relationships, and the global delivery infrastructure to make that shift.

Whether they move fast enough is the real question.

Conclusion

Every major technology transition in the last thirty years has produced the same fear cycle.

People look at what is changing and conclude that what existed before will stop mattering.

Sometimes they are right about specific roles or specific business models becoming obsolete.

But they are almost always wrong about entire industries disappearing.

The Indian IT sector is not a rigid, single-product business.

It is a large, adaptive services industry that has shown (multiple times) that it can reshape itself around whatever enterprises need most at a given point in time.

But the industry will evolve, and there will be pain.

The leadership will also change within the IT Industry.

That is what happened after SaaS. I have reasonable confidence it will happen again.

Have a happy investing.