Introduction

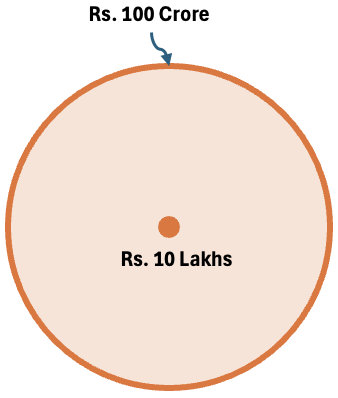

The idea of turning 10 lakhs into 100 crore can sound unreal, right?

For a person who is just starting up, it feels like a cliche, not for real. But a person who has already decoded it in practice, the number growth can be explained using mathematics, market history, and human behaviour.

At this point, it will stop looking magical. The task is demanding, no doubt, but its is possible.

What I’m about to say in this blog post is not shortcuts, lucky trades, or one exceptional stock that changed the luck. It is about time, discipline, and letting compounding do what it is designed to do.

But do you know what the real challenge is? It is not the math. The challenge is staying invested.

What will take you through the journey from 10 lakhs to 100 crore is clear thinking during cycles (up and extreme downs), and behaving sensibly year after year (for demades).

How do I want you to perceive this article? Think of this as a thought experiment that a serious and knowledgeable long-term investor is trying to do.

Imagine that this person, who has the knowledge and experience, had to start again from zero. How would he do it now, in today’s times? No inheritance, no trading, no gambling, pure long-term investing. How will this journey, from 10 lakhs to 100 crore, actually happen?

That is what this blog post tries to answer, without exaggeration or myths.

Table of Contents

- Introduction

- First, understand the mathematics clearly

- 1. Step one is starting with the right mindset

- 2. Asset allocation is next – why equity must dominate early

- 3. Stock selection comes next – Critical Step

- 4. Valuation still matters more than stories

- 5. Reinvestment and discipline: where compounding either survives or dies

- 6. Learning to live with market cycles. Do not fight it

- 7. Position sizing – Here Good Ideas Turn Into Real Wealth

- 8. Time does most of the work, not intelligence

- 9. Is turning 10 lakhs into 100 crore certain?

- 10. Where most people actually fail

- Conclusion

First, understand the mathematics clearly

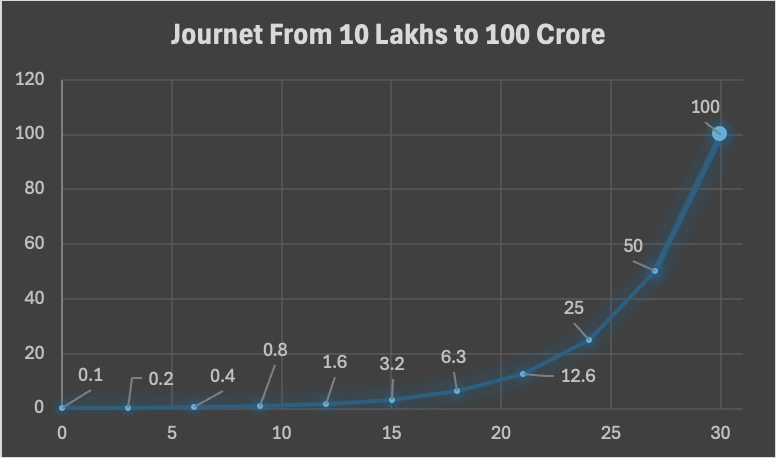

To turn 10 lakhs into 100 crore, you need a 1,000x return. That number looks impossible, but it becomes manageable when you spread it over the time period of 30 years.

If your money doubles every 3 years, this is what happens:

Start: 10 Lakhs:

- 3RD Year: 20 Lakhs

- 6TH Year: 40 Lakhs

- 9TH Year: 80 Lakhs

- 12TH Year: 1.6 Crore

- 15TH Year: 3.2 Crore

- 18TH Year: 6.4 Crore

- 21ST Year: 12.8 Crore

- 24ST Year: 25.6 Crore

- 27TH Year: 51.2 Crore

- 30TH Year: 100 Crore

This way, you will need 10 doubles in 30 Years = ~1,000x.

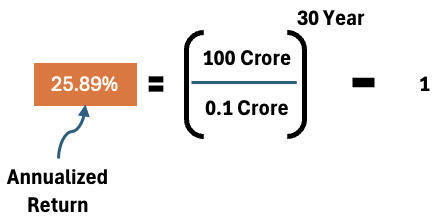

If you want to know the growth rate (CAGR), you will have to use the Compound Interest formula to do the math.

This means you need roughly 25.89% annual compounded returns over 30 years.

Even in India, this is a high return assumption, but it is not a fantasy. If the amount stays invested in quality equity for a period of 30 years, this kind of return is also possible.

The overall Indian equity markets themselves have delivered 14–15% CAGR over long periods. Exceptional investors and focused portfolios have done much better.

But again, I will say that we must get stuck with if 26% CAGR is possible or not. Here, the math is not the hard part; staying on track for 30 years is the real task.

1. Step one is starting with the right mindset

When you begin with 10 lakhs, your real strength is not the money itself. It is the freedom that comes with it.

Small capital allows you to take decisions that larger investors simply cannot take.

You can sit through volatility, make bold bets, and wait patiently without worrying about managing public expectations or large sums.

But this freedom comes with a cost. You have to accept a few realities early on, otherwise the journey becomes frustrating very quickly.

- Your portfolio will swing wildly at times.

- There will be long phases when nothing seems to work.

- And many people around you, friends, relatives, even well-meaning seniors, will think you are being careless or unrealistic.

This is not a process driven by quarterly returns or what others are making in the market.

If you keep checking your progress every day (or every three months), you will lose confidence sooner or later.

Long-term investing works only when you start treating it like a serious, long-duration career, not like a financial product that must perform on demand (deliver results each day).

A simple way to test yourself is this: imagine your portfolio falls 40% in a bad year. Not on paper, actually, falls. Could you still sleep peacefully and stay invested?

If the honest answer is no, then the problem is not the market. The problem is that your mindset is not yet ready for compounding, no matter how good the math looks.

2. Asset allocation is next – why equity must dominate early

For a young investor aiming for outsized compounding, equity is not optional. It is essential.

If you are in your 20s or early 30s, capital preservation is not your primary goal.

Capital growth is.

Debt instruments, fixed deposits, and “balanced” products protect money, but they do not multiply it meaningfully over long periods.

A realistic framework would be:

- Early years: 80–100% equity

- Middle years: Gradual risk moderation

- Later years: Portfolio stabilisation

This is not reckless. It is logical. Time is your biggest risk absorber, and this is how large wealth builders have made their bucks.

3. Stock selection comes next – Critical Step

At some point, you have to be honest with yourself. If your goal is to compound at 25% for decades, simply buying the index and waiting will most likely not get you there.

Index investing is sensible and safe, but it is designed for average outcomes. This journey (10L to 11Cr) is not about average.

What you really need is ownership in a few businesses that keep growing quietly, year after year. Not flashy companies. Not “hot” stocks. Just solid businesses where profits increase steadily, and management does not do anything foolish with shareholder money.

Over time, you start noticing certain patterns.

- Good businesses usually earn much more than what they reinvest.

- They do not keep coming back to shareholders asking for fresh capital.

- Their promoters speak less and execute more.

- And most importantly, their products or services are not dependent on one short-term trend.

Many such businesses emerge from everyday needs, banking, housing finance, consumption, manufacturing, logistics, technology, etc. These sectors may go in and out of favour, but the underlying demand does not disappear. People still save, spend, build, travel, and consume, regardless of market mood.

When evaluating a stock, the question should not be, “Will this go up next quarter?” That is a non-relevant question. A better question is, “Is this business stronger today than it was three years ago?”

If the answer is consistently yes, the stock price usually takes care of itself over time.

This kind of thinking takes patience to develop. In the early years, it is tempting to chase stories and momentum. Everyone does it once.

Long-term investors eventually learns that wealth is built by staying with good businesses long enough. If one keeps jumping from one idea to another, it is not reliable investing.

4. Valuation still matters more than stories

One of the hardest lessons in investing is this: even the best business can disappoint you if you pay the wrong price.

Many investors learn this the hard way. They buy a wonderful company, feel confident about the story, and then spend the next five years wondering why the stock is going nowhere.

Compounding works beautifully only when two things move together:

- The business must keep growing its profits, and

- The valuation must remain sensible.

If earnings rise but the stock was bought at an exaggerated price, the market quietly corrects that mistake over time. You may not lose money, but you lose years.

This is why the concept of a margin of safety is so crucial in real life. The roots of the margin of safety concept lie in simply admitting that we can be wrong. What is the margin of safety? Buying stocks at a price below the price that looks good/fair to you.

Buying at a reasonable price gives you breathing room when growth slows, management makes a mistake, or the market mood turns negative.

Many people think value investing means waiting endlessly for a market crash. That is not practical. Opportunities come even in normal markets, but they require patience. Sometimes the best decision is to watch, track a business, and do nothing for months.

That waiting can feel uncomfortable, especially when others are making quick money, but this is what value investing is. The point is, if you do it correctly, you too can become an investor of the caliber of Warren Buffett or Peter Lynch.

Remember, in stock investing, inactivity is not laziness. It is discipline. Knowing when not to act often protects your capital better than making frequent, confident-sounding decisions.

5. Reinvestment and discipline: where compounding either survives or dies

Compounding does not fail because markets stop working. It fails because money keeps getting pulled out.

This usually happens quietly, so slowly that it is not visible even to us.

A good year in the market, a sudden bonus at work, or a big rally in one stock, and the temptation to “enjoy a little” creeps in. There is nothing wrong with spending money, but timing matters.

If every bull market ends with a bigger car, a fancier phone, or frequent withdrawals from the portfolio, the compounding engine never gets the fuel it needs.

The numbers may look good for a few years, but the long-term curve flattens without you realising it.

Serious investors treat new money differently.

- Dividends are not income to be spent.

- Bonuses are not rewards to be splurged.

- Salary hikes and windfalls are seen as fresh capital to be put back to work.

These actions are not exciting. It will not help you narrate a fancy story on a dinner table with your friends, but something much more important will keep working in the background.

A good habit is to do a quiet check every year. Do not look at how much your portfolio is worth on the screen. Instead, ask yourself this: am I investing more money than last year, or am I slowly taking money out?

Market values go up and down; they do not tell the full story. What really matters is whether the base you are compounding on is growing or not.

If every year you are adding more capital, through savings, dividends, bonuses, or reinvestment, then compounding is working in your favour, even if returns feel dull for a while.

Most people miss this very important point.

In the long run, the investor who keeps increasing the base quietly almost always overtakes the one who chases returns.

6. Learning to live with market cycles. Do not fight it

If you stay invested for 25 or 30 years, the market will test you in every possible way.

- There will be periods when stocks seem to go up every week and everyone suddenly sounds like an expert.

- There will also be long, uncomfortable phases when prices fall, news looks ugly, and your portfolio will refuse to cooperate with your expectations.

Each phase has its own lesson.

- Bull markets tempt you to believe you are smarter than you really are. They reward conviction, but they also punish overconfidence.

- Market corrections, on the other hand, test your patience. This is when doubt creeps in, and even good businesses start looking questionable.

- Sideways markets are perhaps the hardest. Nothing is happening, enthusiasm dies, and even disciplined investors start to find it boring to stay invested.

Over time, successful investors learn one important skill: they adjust their behaviour without abandoning their core beliefs. They may buy less or buy more, slow down or speed up, but they do not panic or reinvent their philosophy every few years.

In investing, the most costly mistakes come from sudden emotional buy or sell calls:

- Selling everything when fear is high and

- Buying when excitement peaks.

At that moment, both can feel logical. But in reality, they quietly destroy years of compounding.

Markets will always move in cycles. The real edge comes from not fighting them and not letting them change who you are as an investor.

7. Position sizing – Here Good Ideas Turn Into Real Wealth

One of the most common reasons investors fail to create meaningful wealth is not a lack of ideas.

It is a lack of conviction.

Many people find good companies, understand the business well, and even buy the stock at the right time, but they never allow the idea to make a real difference to their portfolio.

This usually shows up in the same pattern.

The best ideas are given tiny allocations, while weaker or “experimental” ideas quietly take up equal space. Everything becomes a 1–2% position. When the winner finally plays out, it feels good, but it does not move the needle.

Such a portfolio looks busy; it looks like it did a lot on paper, but the actual progress is not relevant.

Position sizing is not about gambling or putting all your money in one stock. It is about recognising when the odds are genuinely in your favour.

- When you have studied a business,

- Understand its risks,

- Believe in the management, and

- See value in the price,

- That idea deserves more weight than a casual bet or a tip.

This judgment does not come in the first few years. Early on in our investing journey, we must play with caution. Over time, experience teaches you which risks are worth taking and which ones only look exciting on the surface.

Gradually, you learn to back your best ideas a little more confidently, while keeping weaker ideas smaller. This is again one powerful point that experienced portfolio builders will relate to. But this is also true that this step is riskier than all other steps combined; this is why it must be executed only after years of observation and experience.

The uncomfortable truth is this: portfolios do not compound because of average ideas. They compound because a few good decisions are given enough space to work.

Learning how much space to give them is a slow, personal skill. Such a skill will develop only after years of observing (and practicing) both success and regret.

8. Time does most of the work, not intelligence

One of the most misunderstood things about long-term investing is how little brilliance it actually requires.

You do not need to be right all the time. In fact, you will be wrong many times. What matters far more is that a few good decisions are allowed to play out fully, without being interrupted.

If you look at people who have compounded wealth over decades, there is a clear pattern to watch out for.

They did not discover hundreds of winning stocks. They found a handful of good businesses and stayed with them longer than most people felt comfortable doing.

It is the time, not their stock analysis skills, that did the heavy lifting.

This is why calm, patient investors often outperform sharper, more analytical minds.

The smarter investor is tempted to act more; optimize, rebalance, exit early, or move to the next “better” idea. The calmer investor interferes less.

And in investing, less interference often means better outcomes.

9. Is turning 10 lakhs into 100 crore certain?

Of course not.

It is important to say this clearly.

There are no guarantees in markets. This journey is about probability, not promises.

Many things have to go right, and some things will go wrong along the way.

You need to do the following when the results are not visible:

- Long period of high equity exposure,

- The willingness to keep learning, and

- The emotional strength to stay invested when results are not visible.

- You also need consistency. Continue to invest and stay disciplined year after year, even during long phases when returns are poor. During such times, the market will feel boring as there is no excitement or visible progress. But keep investing.

- And yes, luck plays a role. Anyone who denies that in equity investing is being dishonest with the whole process of building wealth.

What this path does not require is secret information, insider access, or extraordinary assumptions.

Our stock markets have already shown, across generations, that disciplined investors can build very large wealth over time. The framework is proven.

What usually breaks down is the human ability to follow it patiently.

10. Where most people actually fail

Most investors understand compounding only intellectually.

Very few can live with it emotionally. How?

- They know that they should hold, but they panic when prices fall.

- They know they should be patient, but get restless when nothing is happening in the stock market for years.

Slowly, small decisions like selling early, chasing trends, and stopping investments will weaken the whole process of building long-term wealth. It is these weak phases when we should be dumping more and more money in quality stocks. No matter how bad the performance, keep investing.

This is why the model rarely fails on paper but fails in real life. Not because the math is wrong, but because human behaviour is inconsistent. We simply do not allow compounding to work to its full potential.

Compounding is simple to understand, but it is not easy to execute. Why? Because human psychology does not support its execution. That is why we have more average people in the world and only a handful of millionaires and billionaires.

Conclusion

Turning 10 lakhs into 100 crore is not about chasing a big number or building a story which we can boast about with friends and family.

It is about building a process that works quietly in the background for 30 years.

Wealth is just the end result of many ordinary decisions done well, again and again.

Most people think too small in the long run and too big in the short run. Three years feels like a lifetime. Thirty years feels unreal (unexecutable).

Compounding works the other way around; it rewards those who think long and act patiently.

So the real question is not whether this journey is possible. The real question is much simpler (and much harder): can you stay disciplined long enough for time to do its job?

Have a happy investing.